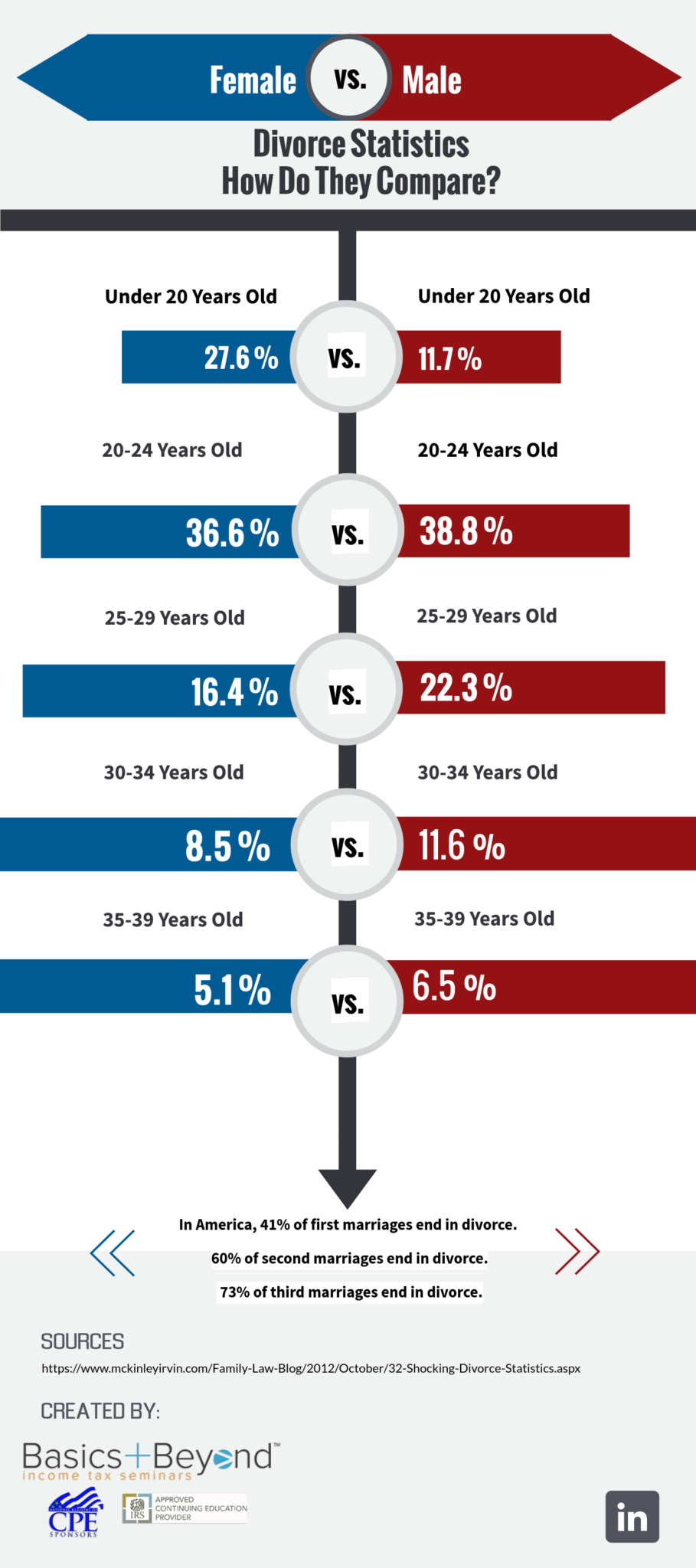

Divorce is a challenging event to experience. Anyone who’s gone through it can attest to just how difficult it can be. And, while most people think it simply won’t ever happen to them, the statistics tend to say otherwise. In fact, as many as 40-50% of marriages in the United States will eventually end in divorce — and those numbers can be even higher for certain segments of the U.S. population. While it’s not exactly an encouraging thought, it’s an important thing to consider: as a CPA or tax professional, there’s roughly a 50/50 chance that any one of your clients’ marriages will ultimately come to an end. And, when that happens, you’ll need to be prepared. Clients will likely look to you for answers about how their divorce will impact their tax filing situation. One of the best ways to keep yourself up to speed with the implication of divorce for your clients’ taxes is by signing up for a tax CPE seminar or tax CPE webinar. Basics & Beyond™ offers a variety of tax CPE options that are updated on an annual basis to reflect recent changes to the tax code, especially in light of the new 2018 tax reform legislation.

Divorce is a challenging event to experience. Anyone who’s gone through it can attest to just how difficult it can be. And, while most people think it simply won’t ever happen to them, the statistics tend to say otherwise. In fact, as many as 40-50% of marriages in the United States will eventually end in divorce — and those numbers can be even higher for certain segments of the U.S. population. While it’s not exactly an encouraging thought, it’s an important thing to consider: as a CPA or tax professional, there’s roughly a 50/50 chance that any one of your clients’ marriages will ultimately come to an end. And, when that happens, you’ll need to be prepared. Clients will likely look to you for answers about how their divorce will impact their tax filing situation. One of the best ways to keep yourself up to speed with the implication of divorce for your clients’ taxes is by signing up for a tax CPE seminar or tax CPE webinar. Basics & Beyond™ offers a variety of tax CPE options that are updated on an annual basis to reflect recent changes to the tax code, especially in light of the new 2018 tax reform legislation.

That said, we’ve put together this blog post to summarize some of the biggest things that will need to be considered following a divorce when tax time rolls around. Keep reading to learn more.

How Divorce Can Impact Your Taxes

It’s fair to say that taxes probably aren’t the first thing people worry about after filing for divorce. A lot can change when it comes to tax filing post-divorce, though, and it’s important to take all of these items into account.

Child Support

Before a divorce, there’s likely little reason to think about child support (unless one member of a marriage couple is has already been through a prior divorce involving children). However, if you have kids and are going through a divorce, child support is likely to come up.

The tax ramifications of child support are quite straightforward, though. Put simply, child support is neither deductible nor is it taxable as income. In other words, whether you’re paying child support out or receiving it from your ex, it won’t have any real impact on your taxes.

Alimony

Alimony is another story, however. While you aren’t able to deduct child support payments from your taxes, in the past it was possible to deduct alimony as an expense. In fact, you could deduct alimony even if you don’t itemize your deductions.

What changed? Why are we speaking in the past tense here? Well, the new 2018 tax bill has determined that alimony will no longer be deductible. There’s another change, too: whereas alimony used to be included in the recipient’s gross income, that’s no longer the case, either. Instead, alimony will now be taxable at the tax rate of the person making the payments. In other words, if the payor of the alimony is taxed at a very high marginal tax rate — say, 32% — but the payee’s marginal rate is much lower — perhaps only 12% or 22% — the alimony payments will be taxed at the 32% rate, regardless of the payee’s marginal tax rate. To learn more about the details of these new changes, consider signing up for one of our tax CPE webinars.

IRA Deductions and Transferred Retirement Assets

In determining whether contributions to your spouse’s IRA are deductible, you have to examine whether you received a “final decree of divorce or separate maintenance” before the end of the tax year in question. If you did, then you can’t deduct any of the contributions you made to your ex’s IRA on that year’s tax return.

In some instances, a divorcing couple will initiate a transfer of certain retirement assets. For example, you might opt to transfer some of your 401(k) savings out of your account and over to your former spouse. In some cases, this can be considered a taxable distribution. As a result, you might have to pay taxes on these funds. This can be avoided, though: do your best to initiate the transfer as part of a Qualified Domestic Relations Order (QDRO). This can allow your ex to have access to your retirement fund, without you have to pay taxes on any kind of distribution. Rather than paying taxes on the sum, your former spouse should be able to roll the distribution over as though they were an employee receiving a plan distribution and rolling it over to the following tax year.

Dependents and Exemptions

As a married couple filing jointly, your child would have been claimed as a dependent on your joint tax return for exemption purposes. However, in general, it’s only possible to claim a child on one tax return. This means that once you’re divorced, you’ll no longer be able to claim your child as a dependent on both of your income taxes. Once you’re filing separately, only one of your will be able to claim children as dependents.

As you can imagine, this can be quite problematic for parents who are sharing custody of children. After all, whichever parent is able to claim a dependent child exemption also gets the $1,000 per child tax credit (assuming their income level allows them to qualify), and this amount is going up to as much as $2,000 per child following the recent changes to the tax code in 2018.

Generally speaking, the so-called “custodial parent” is the one who is allowed to claim a child on their tax return. This will usually be spelled out in court proceedings related to custody. However, if neither parent is the “custodial parent,” then the parent who’s able to claim a child on their taxes will typically be the one who had custody of the child for a larger number of days in any given tax year.

When both parents attempt to claim a child as a dependent and feel they have an equal claim to do so, the IRS uses a set of tiebreaker rules to determine which parent will actually be allowed to claim their child as a dependent. These rules include a number of tests: the relationship test; the residence test; the income test; and more. While we don’t have time to go into all of these rules here, they’re covered in some of our tax CPE webinars.

Sale of a Home

If you and your spouse owned a home jointly and opt to sell it as part of your divorce proceedings, you might be subject to capital gains taxes. As a rule, you can deduct up to the first $250,000 of your home sale if the house in question was your primary home, and if you lived there for at least 2 out of the past 5 years. A married couple filing jointly can increase this amount to $500,000.

If you sell your home post-divorce, this $500,000 number still effectively applies. Why? Because both you and your former spouse can claim $250,000 each in exemption on your individual income tax returns. If you receive the home in a divorce and opt to sell it later down the road, though, you’ll still be entitled to the $250,000 exclusion.

Your Filing Status

One of the most confusing things for divorcing or newly divorced couples centers around the question of their filing status. While married, you likely filed a joint return with your spouse. This is standard practice for the vast majority of married couples (although some couples do opt to file as “married filing jointly”).

If you’re not divorced by the end of the tax year, you can file jointly for that tax year. However, once your divorce is actually finalized, you will no longer be able to file a joint return. Once that happens, you’ll likely have the option of filing as head of household. This can be advantageous for a number of reasons. First off, you’ll be entitled to a higher standard deduction. On top of that, though, the cap for each tax bracket changes for head of household versus filing single. In order to qualify for a head of household filing, you’ll need to have had at least one dependent (such as your child) living with you for more than half of the year. In other words, you’ll need to be able to claim your child or children on your tax return. You also will need to have been responsible for more than half of the expenses of maintaining your household. If you don’t meet all of these requirements, you’ll probably have to file as single following your official divorce.

If you have clients who have been through divorce and are filing as head of household, changes to the tax code as part of the new tax bill could have a direct impact on them. Consider taking one of our 2018 tax CPE webinars to bring yourself up to speed on these important changes.

Medical Bills and Medical Expenses

There are few things in life more stressful than being hit with major medical bills. While an excellent insurance policy can do a lot to minimize the potential financial impact of a medical emergency, many plans require you to pay a significant amount in the form of a deductible or coinsurance. These kinds of expenses are very difficult to plan or budget for, and otherwise healthy individuals are sometimes blindsided by them as the result of an unexpected accident or the sudden onset of an illness.

The ability to deduct these expenses from your federal taxes can save you a significant amount of money. While it’s obviously possible to deduct your own medical expenses following a divorce, it may be less obvious how the deduction of medical bills works when it comes to your child. Simply put: if you’re paying your child’s medical bills following your divorce, you can generally deduct those bills as part of your taxes (assuming you itemize your deductions). It doesn’t matter if your former spouse has custody of and/or claims your child as a dependent on their federal income tax return. Regardless, the person who’s actually paying that child’s medical expenses is the one who is allowed to claim those expenses as a deduction when filing their individual income taxes.

Other Tax Credits You Can Claim

If you or a client has recently been through a divorce, you might be wondering: are there any other deductions that can be claimed on my tax return? We’ve talked about quite a few of the more obvious ones here, including medical bills, capital gains exemption for the sale of a home, the child tax credit, and more. Here’s one more than you might not have thought of, though.

As we discussed earlier, the parent who claims the child as a dependent on their tax return is able to take the child tax credit for that child. However, even if your former spouse claims your child as a dependent when filing taxes, you may still be eligible to claim the childcare tax credit for any expenses you incur as the result of childcare that allow you to work. In other words, if you’re paying for childcare in order to hold down a job, you can generally claim those childcare expenses even if you’re not able to claim your child as a dependent on your federal income tax return. Considering the rising costs of child care, this can be a significant amount of money in many instances — even if you have custody of your child less than 50% of the time.

Taxable Assets as the Result of the Divorce

It’s common for divorce settlements to involve the transfer of assets from one party to the other. When this happens, there’s generally little to worry about come tax time. This is due to the fact that the beneficiary of an asset transfer that comes as the result of a divorce is generally not required to pay taxes on those assets.

Remember, though: the tax basis of an asset shifts when it is transferred. For example, if you opt to sell a house down the road that you’ve received as part of a divorce settlement, any capital gains tax you have to pay (after the $250,000 individual exemption) will be based on the asset’s appreciation both before and after your divorce. As a result of this, it’s important to think about the tax basis for an asset as well as the asset’s value itself when it comes to calculating your divorce settlement.

Changing Your Name

Many people choose to change their last name following a divorce. If you opt to do the same, you’ll want to notify the Social Security Administration immediately about the change. This is because the name on your tax return needs to match both IRS’s records as well as the Social Security Administration’s. If the two don’t match, your return may be rejected. You’ll then have to re-file a paper return, which can cause various problems associated with your tax timeline.

Tax CPE Webinars for Divorce and Its Tax Implications

Basics & Beyond offers tax CPE webinars covering the latest in changes to the tax code, including tax topics related to post-divorce filing for formerly married couples. Take a look at our 2018 tax CPE topics and sign up today!