Stay Informed with the June 2024 Tax Newsletter

In this Issue:

- Watch Out for These Current Scams

- Tax Pros: Use Current Version of Offer in Compromise Booklet

- To Protect Against Identity Theft, IRS Adds Additional Protectionsto Centralized Authorization File, Transcript Delivery System; Changes Designed to Protect Sensitive Tax Pro, Taxpayer Information

- Procedures for §355 PLR Requests Updated

- Home Improvements Could Help Taxpayers Qualify for Home Energy Credits

- HSA 2025 Inflation Adjustments

- How to Request Help with a Tax Matter from the IRS Independent Office of Appeals

- CAF Numbers in “Pending Review” Status

- What Taxpayers Should Do if They Receive Mail from the IRS

- IRS Announces Extension of Free File Program Through 2029

- S. Taxpayers Living and Working Abroad Face June 17 Deadline to File their 2023 Tax Returns

- Applicable Federal Rates for June 2024, Rev. Rul. 2024-12

Issue 1: Watch Out for These Current Scams

The IRS issued a consumer alert following ongoing concerns about a series of tax scams and inaccurate advice on social media that have encouraged thousands of taxpayers to file fictitious refund claims this past tax season.

The scams involve the Fuel Tax Credit, the Sick and Family Leave Credit and household employment taxes. Suspicious claims have resulted in refund delays and IRS requests for documentation. Taxpayers who erroneously filed for these claims should follow the advice in the letters and amend their returns.

For taxpayers who did fall for these traps, they need to follow steps to verify their eligibility for the claim. Some taxpayers could also face steep financial penalties, potential follow-up audits or criminal action for improper claims. The IRS encourages people to review the guidelines, talk to a trusted tax preparer and, in some cases, file an amended return to remove claims for which they’re ineligible to avoid potential penalties.

The bad claims were caught during the IRS fraud review process. Taxpayers who filed these claims should realize they have been tricked, and they face an extensive review process and a long potential wait if they are owed a refund for other things.

Problem claims involve Fuel Tax Credit, Sick and Family Leave Credit, Household Employment Taxes.

The IRS has identified three common themes that continue to pop up among these bad refund claims. They involve legitimate tax provisions, but they are limited to very specialized situations. The vast majority of the related claims coming in does not qualify:

Fuel Tax Credit: This specialized credit is designed for off-highway business and farming use. Taxpayers need a business purpose and a qualifying business activity such as running a farm or purchasing aviation gasoline to be eligible for the credit. Most taxpayers do not qualify for this credit.

Credits for Sick Leave and Family Leave: This specialized credit is available for self-employed individuals for 2020 and 2021 during the pandemic; the credit is not available for 2023 tax returns. The IRS is seeing repeated instances where taxpayers are incorrectly using Form 7202, Credits for Sick Leave and Family Leave for Certain Self-Employed Individuals, to incorrectly claim a credit based on income earned as an employee and not as a self-employed individual.

Household Employment taxes: Taxpayers “invent” fictional household employees and then file Schedule H (Form 1040), Household Employment Taxes, to claim a refund based on false sick and family medical leave wages they never paid.

Given the questionable nature of many of these claims, the IRS has frozen the refunds for these taxpayers. Taxpayers have to follow several specific steps to resolve these issues.

Taxpayers whose refunds have been frozen will generally receive one of several letters from the IRS asking for additional information.

Initially, taxpayers may have received a letter asking them to verify their identity. In these situations, if they filed the return in question, they should review whether their tax return is accurate. For example, did they actually qualify for one of the three credits listed above? Or if they used a tax preparer, check to see if the preparer actually signed the tax return. When tax preparers do not sign a tax return, it is a red flag that the taxpayer is being misled.

Taxpayers who improperly claimed these credits do not need to visit a Taxpayer Assistance Center (TAC) to verify their identity. However, they may need to amend their tax return to remove the improperly claimed credit.

A number of taxpayers who initially received correspondence asking about their identity may be receiving an additional letter seeking additional documentation to show they actually qualify for the credits they claimed. Taxpayers who verified their identity in-person may receive these letters. Taxpayers who have not verified their identity yet and receive one of these letters asking for additional documentation should follow the advice in the most recent letter.

These letters – IRS Notice 3176c – apply to potentially frivolous tax returns, which includes incorrect claims for Fuel Tax Credits, Sick and Family Leave Credits and Household Employment taxes.

Legitimate taxpayers qualifying for these credits can submit documentation showing they actually qualify for the credit. But people who do not qualify for these credits risk facing a penalty of up to $5,000 per return for filing a frivolous claim. Taxpayers submitting inaccurate claims also face the risk of an audit. Those who knowingly filed a false tax return also face potential criminal prosecution.

To avoid penalties and potential follow-up action by the IRS, taxpayers who incorrectly filed for these claims need to promptly submit an accurate tax return without the claims.

The IRS noted that the entire refund amount is frozen on returns with these bad claims. Taxpayers will not receive any portion of their refund, even if they also claimed legitimate credits.

Issue 2: Tax Pros: Use Current Version of Offer in Compromise Booklet

The IRS recently released its April 2024 version of the Form 656-B, Offer in Compromise Booklet. Tax professionals should always download and use the most current version of this form to avoid processing delays. The booklet also includes the forms taxpayers must complete as part of the Offer-in-Compromise (OIC) process. An OIC lets a taxpayer settle their tax debts for less than the full amount once the taxpayer has exhausted all other payment options. The IRS will consider each taxpayer’s unique set of facts and circumstances before accepting an OIC.

Issue 3: To Protect Against Identity Theft, IRS Adds Additional Protections to Centralized Authorization File, Transcript Delivery System; Changes Designed to Protect Sensitive Tax Pro, Taxpayer Information

With identity theft and refund fraud an ongoing concern, the Internal Revenue Service has highlighted additional protections for tax professionals being taken to increase security for the Centralized Authorization File (CAF) program and placed new guidelines on requesting client transcripts by phone.

The IRS has become increasingly concerned about the risk a compromised CAF number presents to tax professionals and taxpayers. In these cases, there is risk that fraudsters could use a compromised CAF to obtain transcripts and other sensitive taxpayer personally identifiable information (PII) to commit identity theft refund fraud and other crimes. In many cases, the fraudster has not only obtained a practitioner’s CAF number but also has the practitioner’s sensitive personal information.

To address this issue, the IRS has a process in which suspected compromised CAF numbers are placed into a suspended status pending further review. Once placed into a suspended status, the owner of the CAF number will be contacted to confirm if the CAF number has been compromised. If the compromise is confirmed, the IRS will take the appropriate actions to address the compromised CAF number. The IRS recognizes the significance of the CAF process and is continuously working on ways to expedite this review process for impacted practitioners.

In addition to the changes being made to protect tax professionals from a compromised CAF number, the IRS has also taken related security steps to change how tax professionals can order transcripts by phone through the Transcript Delivery System (TDS).

Tax professionals now need to call the Practitioner Priority Service (PPS) line to request transcripts to be deposited into their Secure Object Repository (SOR) mailbox. IRS employees on other phone lines may not be authorized to provide transcripts through the SOR delivery method. Tax professionals will need to pass enhanced authentication. If the identity of the caller cannot be verified, transcripts will not be delivered using the SOR delivery method but will instead be mailed to the taxpayer’s address of record.

Tax professionals should also be on the lookout for unsolicited scam emails asking to provide credential information such as CAF number, Electronic Filing Identification Number (EFIN) information and driver’s license. These emails may look like they are coming from the IRS or a tax software company. Tax professionals who receive these unsolicited emails should report them to [email protected].

Issue 4: Procedures for §355 PLR Requests Updated

The IRS has issued Revenue Procedure 2024-24 to update the process taxpayers must use to request private letter rulings (PLRs) regarding certain matters related to §355 transactions. § 355 allows corporations that meet certain requirements to distribute stock and securities in a controlled corporation to its shareholders and security holders without the recipients recognizing gain or loss.

The updated procedures address such matters as representations, information and analysis that must be submitted with the PLR requests. The IRS also issued Notice 2024-38, which seeks public feedback on the provisions set out in the revenue procedure and explains the Treasury Department’s and IRS’s views and concerns regarding some matters included in the procedure.

Issue 5: Home Improvements Could Help Taxpayers Qualify for Home Energy Credits

The Internal Revenue Service reminds taxpayers that making certain energy efficient updates to their homes could qualify them for home energy credits.

The credit amounts and types of qualifying expenses were expanded by the Inflation Reduction Act of 2022. Taxpayers who make energy improvements to a residence may be eligible for home energy tax credits.

Taxpayers can claim the Energy Efficient Home Improvement Credit and the Residential Clean Energy Credit for the year the qualifying expenditures are made. Homeowners who improve their primary residence will find the most opportunities to claim a credit for qualifying expenses. Renters may also be able to claim credits, as well as owners of second homes used as residences. Landlords cannot claim this credit.

IRS encourages taxpayers to review all requirements and qualifications at IRS.gov/HomeEnergy for energy efficient equipment prior to purchasing. Additional information is available on energy.gov, which compares the credit amounts for tax year 2022 and tax years 2023-2032.

Energy Efficient Home Improvement Credit

Taxpayers that make qualified energy-efficient improvements to their home after Jan. 1, 2023, may qualify for a tax credit up to $3,200.

As part of the Inflation Reduction Act, beginning Jan. 1, 2023, the credit equals 30% of certain qualified expenses:

- Qualified energy efficiency improvements installed during the year which can include things like:

- Exterior doors, windows and skylights.

- Insulation and air sealing materials or systems.

- Residential energy property expenses such as:

- Natural gas, propane or oil water heaters.

- Natural gas, propane or oil furnaces and hot water boilers.

- Heat pumps, water heaters, biomass stoves and boilers.

- Home energy audits of a main home.

The maximum credit that can be claimed each year is:

- $1,200 for energy property costs and certain energy efficient home improvements, with limits on doors ($250 per door and $500 total), windows ($600) and home energy audits ($150).

- $2,000 per year for qualified heat pumps, biomass stoves or biomass boilers.

The credit is nonrefundable which means taxpayers cannot get back more from the credit than what is owed in taxes and any excess credit cannot be carried to future tax years.

Residential Clean Energy Credit

Taxpayers who invest in energy improvements for their main home, including solar, wind, geothermal, fuel cells or battery storage, may qualify for an annual residential clean energy tax credit.

The Residential Clean Energy Credit equals 30% of the costs of new, qualified clean energy property for a home in the United States installed anytime from 2022 through 2032.

Qualified expenses include the costs of new, clean energy equipment including:

- Solar electric panels.

- Solar water heaters.

- Wind turbines.

- Geothermal heat pumps.

- Fuel cells.

- Battery storage technology (beginning in 2023).

Clean energy equipment must meet the following standards to qualify for the Residential Clean Energy Credit:

- Solar water heaters must be certified by the Solar Rating Certification Corporation, or a comparable entity endorsed by the applicable state.

- Geothermal heat pumps must meet Energy Star requirements in effect at the time of purchase.

- Battery storage technology must have a capacity of at least 3 kilowatt hours.

This credit has no annual or lifetime dollar limit except for fuel cell property. Taxpayers can claim this credit every year they install eligible property on or after Jan. 1, 2023, and before Jan. 1, 2033.

This is a nonrefundable credit, which means the credit amount received cannot exceed the amount owed in tax. Taxpayers can carry forward excess unused credit and apply it to any tax owed in future years.

Additional information is available at IRS.gov on qualifying residences and information for taxpayers who also use their home for a business.

When it is time to file a tax return, taxpayers can use Form 5695, Residential Energy Credits, to claim the credit. This credit must be claimed for the tax year when the property is installed, not just purchased.

Good Record Keeping

Taxpayers are encouraged to keep good records of purchases and expenses. This will assist in claiming the applicable credit during tax filing season.

Issue 6: HSA 2025 Inflation Adjustments

Revenue Procedure 2024-25 provides the 2025 inflation adjusted amounts for Health Savings Accounts (HSAs) as determined under § 223 of the Internal Revenue Code and the maximum amount that may be made newly available for excepted benefit health reimbursement arrangements (HRAs) provided under § 54.9831-1(c)(3)(viii) of the Pension Excise Tax Regulations.

(1) Annual contribution limitation.

For calendar year 2025, the annual limitation on deductions under § 223(b)(2)(A) for an individual with self-only coverage under a high deductible health plan is $4,300.

For calendar year 2025, the annual limitation on deductions under § 223(b)(2)(B) for an individual with family coverage under a high deductible health plan is $8,550.

(2) High deductible health plan.

For calendar year 2025, a “high deductible health plan” is defined under § 223(c)(2)(A) as a health plan with an annual deductible that is not less than $1,650 for self-only coverage or $3,300 for family coverage, and for which the annual out-of-pocket expenses (deductibles, co-payments, and other amounts, but not premiums) do not exceed $8,300 for self-only coverage or $16,600 for family coverage.

For plan years beginning in 2025, the maximum amount that may be made newly available for the plan year for an excepted benefit HRA under § 54.9831-1(c)(3)(viii) is $2,150. See § 54.9831-1(c)(3)(viii)(B)(1) for further explanation of this calculation.

Issue 7: How to Request Help with a Tax Matter from the IRS Independent Office of Appeals

If a taxpayer disagrees with an IRS decision, they can ask the IRS Independent Office of Appeals to review their case. This office is separate from the rest of the IRS. Appeals officers review cases that taxpayers submitted, meet with the taxpayer informally and consider the taxpayer’s position and the IRS’s position in a fair and unbiased manner.

Overview of the appeals process

Here’s what taxpayers need to know if they want to appeal their case:

- To submit an appeal request, taxpayers mail their request in writing to the office that sent them the letter with their appeal rights. For information on filing a formal written protest or a small case request, taxpayers should review Publication 5, Your Appeal Rights and How To Prepare a Protest If You Disagree. The IRS office that receives the request will consider the taxpayer’s request and attempt to resolve the disputed tax issues. If that office can’t resolve the taxpayer’s issues, they will forward the case to Appeals for consideration.

- Once the request is with Appeals, the Appeals officer contacts the taxpayer within 45 days by mail to schedule an informal conference to review the taxpayer’s situation. Appeals conducts conferences by phone, in person and by video. Taxpayers may choose which type of conference they prefer.

- At the conference, the Appeals officer discusses with the taxpayer the law as it applies to the facts of the case, including court rulings on similar cases.

- If a taxpayer has not heard about their appeal and it’s been more than 120 days since they filed their request, taxpayers can ask for a status update by contacting the IRS office they worked with last.

- If the taxpayer sends new information or documents to Appeals, the Appeals officer may need to send the case back to the original IRS office to review the new information. Appeals will not raise new issues or reopen issues agreed to by the taxpayer or the IRS except in cases of potential fraud or malfeasance.

- Appeals officers review the facts, the law, the taxpayer’s comments and information the taxpayer and the IRS office presented before they make a final decision. They will also explain to the taxpayer the reasons for the decision and their options. Generally, there are three outcomes of an appeal:

- In the IRS’s favor: If the facts and laws support the government’s position, the Appeals officer recommends that the taxpayer concede and give up the issue.

- In the taxpayer’s favor: If the law and facts support the taxpayer’s position or courts have ruled in favor of taxpayers in similar cases, the Appeals officer recommends that the IRS concede and give up the issue.

- Compromise: The Appeals officer may recommend a compromise when the facts or laws are unclear, or the courts have made different rulings on similar cases. In this situation, Appeals may recommend a settlement where the taxpayer pays a percentage of the tax due.

Interest continues to add up on any unpaid balance a taxpayer owes as appeals reviews a case.

Issue 8: CAF Numbers in “Pending Review” Status

To fulfill their professional obligations, practitioners—attorneys, certified public accountants, enrolled agents, and tax return preparers who participate in the Internal Revenue Service’s Annual Filing Season Program—must comply with Circular 230, Regulations Governing Practice before the Internal Revenue Service (31 CFR Subtitle A, Part 10), which is administered and enforced by the IRS’s Office of Professional Responsibility (OPR). Only the OPR has authority to suspend or revoke, through disbarment, a practitioner’s eligibility and authority to practice before the IRS.

A prerequisite to representing a taxpayer before the IRS is filing a Form 2848, Power of Attorney and Declaration of Representative. Validly completed authorizations, which specify the tax periods and taxes to which they relate, are recorded on the IRS’s Central Authorization File (CAF).

To prevent unauthorized disclosure of taxpayer information, in certain circumstances a practitioner’s CAF number may be suspended pending an IRS review into whether the CAF number has been compromised owing to identity theft or other fraud. This article provides background on the IRS’s procedures relating to suspended CAF numbers, including how an affected practitioner can expedite the resolution of a CAF number review.

What Is a CAF Number and Why Is It Important?

To enhance taxpayer confidentiality and to facilitate interaction between practitioners and IRS personnel, each practitioner is assigned a nine-digit CAF number. CAF numbers, which are different from a tax professional’s preparer tax identification number (PTIN) or their Social Security number (SSN), are used by the IRS to determine and verify the extent of a practitioner’s authority to represent a taxpayer before the IRS and receive and inspect the taxpayer’s confidential tax information.

The IRS also uses CAF numbers to fulfill and keep track of requests for client information (like transcripts) while safeguarding both the client’s and the tax professional’s personal information. Thus, consistent with the taxpayer privacy provisions of § 6103, IRS employees will check the CAF to ensure they are dealing only with someone with actual authority to act on behalf of a taxpayer and to request disclosure of the taxpayer’s return information. The CAF number itself is personal identifiable information (PII) and should, as much as possible, be kept secure.

What Might Cause a CAF Number to Be Placed in “Pending Review” Status?

Given the sensitivity of taxpayer information, the IRS is continually reviewing and strengthening its practices to guard against identity theft and the improper disclosure of taxpayer information. In connection with those effort to authenticate an individual’s identity and authorization to receive sensitive information, the IRS has long requested personal information, in addition to their CAF number, from practitioners (or anyone accessing tax-related information by means of a Form 8821). The purpose of the authentication process, including the validation of the individual’s SSN, is to protect both taxpayers and the tax professionals who are working on their behalf.

Beyond this basic authentication step, the IRS has a process for IRS employees to refer authorizations with suspicious characteristics for further review. Under this process, the status of the affected CAF account will be coded to “P” for “pending review,” indicating that the CAF number is currently under review for potential compromise and may be subject to fraudulent use. To safeguard taxpayer information pending the review, the practitioner to whom the CAF number was assigned will be unable to rely on the CAF or IRS employees to authenticate the practitioner’s authority to represent taxpayers until the review process is complete.

For security reasons, IRS customer service representatives assigned to the Practitioner Priority Service (PPS), or other call sites cannot, for example, interact with the practitioner about a represented taxpayer’s tax matter. The process is akin to the freeze that a credit card company imposes when their fraud-prevention measures are activated, though for a compromised CAF number, the confidential information of multiple clients as well as the practitioner could be at stake.

First, the suspension may have absolutely nothing to do with anything the practitioner has done. If the practitioner has included their CAF number in a document appropriately shared with a client or other third party and that document (e.g., a copy of a Form 2848 or Form 8821) is exposed because of a physical or digital data breach experienced by the client or third party, the CAF number could be compromised and misused—in particular, by a malicious actor who files a fraudulent authorization form with the IRS to gain access to taxpayer information. In addition, there could be aspects of a practitioner’s tax practice that, while legitimate, might trigger IRS red flags.

The line between actual fraudulent use of a CAF number and its mere appearance can be very thin, as can the line between a compromised number and one that is uncompromised but has anomalous yet innocuous attributes. As a result, “false positives” sometimes occur, with practitioners’ legitimate, uncompromised CAF numbers being suspended pending review.

A practitioner may learn that this has happened to them in different ways. For example, they might contact the IRS to discuss a client’s tax matter and be informed that the conversation cannot occur because the practitioner’s authority to represent the client cannot be verified. Regrettably, because of privacy concerns or other restrictions, the IRS employee who is dealing with the practitioner (or the taxpayer) may not be able to share any additional information with them, only exacerbating their confusion.

Once a preliminary determination is made that a practitioner’s (or other tax professional’s) CAF number may have been compromised and is placed in review, the practitioner will receive a letter by mail from the IRS—generally from IRS Criminal Investigation (CI) —letting them know their CAF is under review.

To help expedite the review process:

- The individuals who receive these letters are asked to verify their identities by sending to the IRS a notarized document that includes pictures of their photo identification.

- The notarized document should be returned to Criminal investigation (CI) using the mailbox provided in the letter within 30 days from the date of the letter.

- The return of the notarized document will then begin a dialogue of verifying their client listings and, if needed, the issuance of a new CAF number. The dialogue may be done over the phone in some cases to accelerate the process.

For those CAF holders whose CAF number is confirmed to be compromised, the IRS will work with the CAF holder to assign them a new CAF number and move their clients to the tax professional’s new CAF number.

The holders of all CAF numbers currently coded as “pending review” have been contacted. The individuals who are told that their CAF account is in “pending review” status can contact the IRS directly by email at [email protected].

Protecting confidential taxpayer data is of paramount concern to the IRS. At the same time, the IRS recognizes that suspending a CAF number pending review can have significant effects on a practitioner’s ability to provide valuable services to their clients. For these reasons, the IRS is continually working to identify, adopt, and refine procedures to detect, address, and prevent actual or possible fraud.

Notably, the IRS recently implemented new security measures applicable to how tax professionals can order by phone tax transcripts generated through the Transcript Delivery System (TDS). Tax professionals will now need to call the PPS line to request transcripts be deposited into the professional’s Secure Object Repository (SOR) mailbox. Transcripts will only be provided via phone contact with the PPS; IRS employees on other phone lines may no longer be authorized to provide transcripts through the SOR delivery method. When they call the PPS, tax professionals will need to pass currently required authentication and verify the Short Identification (ID) number associated with their SOR mailbox.

With these new measures, the OPR intends for the IRS to explore ways that may improve the resolution process for potentially compromised CAF numbers and minimize the burden imposed on practitioners.

Typically, CAF numbers are assigned when the practitioner files their first authorization with the IRS. Practitioners may, however, inadvertently be assigned additional CAF numbers if they fail to include their CAF number on an authorization filed with the appropriate CAF unit. To avoid unintended additional CAF numbers, practitioners are encouraged to include their CAF number on all later authorizations.

If the IRS concludes that a CAF number is, in fact, compromised, the CAF status will be recoded to “Confirmed Fraud.” Attempts to access taxpayer data using a CAF number with a status of “confirmed fraud” will be unsuccessful.

Issue 9: What Taxpayers Should Do if They Receive Mail from the IRS

Recently we were contacted by a taxpayer concerning a letter/notice they had received from IRS. The taxpayer was not our client but was concerned about the advice their preparer provided – not to respond as the IRS makes all sorts of mistakes and since it was IRS’s fault – they will figure it out.

This is probably the worse advice you can provide a client. Depending on the notice/letter and what the issue is you should respond unless the notice/letter specifically tells you not to. Typically, a taxpayer will need to act only if they do not agree with the information if the IRS asked for more information or if they have a balance due.

IRS sends notices and letters when it needs to ask a question about a taxpayer’s federal tax return, let them know about a change to their account or request a payment. Do not panic if something comes in the mail from the IRS – they are here to help.

When a taxpayer receives mail from the IRS, they should:

Read the letter carefully. Most IRS letters and notices are about federal tax returns or tax accounts. Each notice deals with a specific issue and includes any steps the taxpayer needs to take. A notice may reference changes to a taxpayer’s account, taxes owed, a payment request or a specific issue on a tax return. Taking prompt action could minimize additional interest and penalty charges.

Review the information. If a letter is about a changed or corrected tax return, the taxpayer should review the information and compare it with the original return. If the taxpayer agrees, they should make notes about the corrections on their personal copy of the tax return and keep it for their records.

Take any requested action, including making a payment. The IRS and authorized private debt collection agencies do send letters by mail. Taxpayers can also view digital copies of select IRS notices by logging into their IRS Online Account. The IRS offers several options to help taxpayers struggling to pay a tax bill.

Reply only if instructed to do so. Taxpayers do not need to reply to a notice unless specifically told to do so. There is usually no need to call the IRS. If a taxpayer does need to call the IRS, they should use the number in the upper right-hand corner of the notice and have a copy of their tax return and letter.

Let the IRS know of a disputed notice. If a taxpayer does not agree with the IRS, they should follow the instructions in the notice to dispute what the notice says. The taxpayer should include information and documents for the IRS to review when considering the dispute.

Keep the letter or notice for their records. Taxpayers should keep notices or letters they receive from the IRS. These include adjustment notices when the IRS acts on a taxpayer’s account. Taxpayers should keep records for three years from the date they filed the tax return.

Watch for scams

The IRS will never contact a taxpayer using social media or text message. The first contact from the IRS usually comes in the mail.

In the case I assisted with, we gained a new client, but we also acted and provided the information requested. If we had not responded the client would have been charged additional tax as well as interest and penalties which they should not have owed. Once we provided the information which required some research, we were able to solve the issue.

Letter/notices are the first line of communication with the taxpayer. They are not to be ignored in most cases.

Issue 10: Year-round Tax Planning Pointers for Taxpayers

Here are some simple things taxpayers can do throughout the year to make filing season less stressful.

Organize tax records. Create a system that keeps all important information together. Taxpayers can use a software program for electronic recordkeeping or store paper documents in clearly labeled folders. They should add tax records to their files as they receive them. Organized records will make tax return preparation easier and may help taxpayers discover overlooked deductions or credits.

Identify filing status. A taxpayer’s filing status determines their filing requirements, standard deduction, eligibility for certain credits and the correct amount of tax they should pay. If more than one filing status applies to a taxpayer, they can get help choosing the best one for their tax situation with the IRS’s Interactive Tax Assistant, What Is My Filing Status. Changes in family life — marriage, divorce, birth and death — may affect a person’s tax situation, including their filing status and eligibility for certain tax credits and deductions.

Understand adjusted gross income (AGI). AGI and tax rate are important factors in figuring taxes. AGI is the taxpayer’s income from all sources minus any adjustments. Generally, the higher a taxpayer’s AGI, the higher their tax rate and the more tax they pay. Tax planning can include making changes during the year that lower a taxpayer’s AGI.

Check withholding. Since federal taxes operate on a pay-as-you-go basis, taxpayers need to pay most of their tax as they earn income. Taxpayers should check that they’re withholding enough from their pay to cover their taxes owed, especially if their personal or financial situations change during the year. To check withholding, taxpayers can use the IRS Withholding Estimator. If they want to change their tax withholding, taxpayers should provide their employer with an updated Form W-4.

Make address and name changes. Taxpayers should notify the United States Postal Service, employers and the IRS of any address change. To officially change a mailing address with the IRS, taxpayers must compete Form 8822, Change of Address, and mail it to the correct address for their area. For detailed instructions, see page 2 of the form. Report any name change to the Social Security Administration. Making these changes as soon as possible will help make filing their tax return easier.

Save for retirement. Saving for retirement can also lower a taxpayer’s AGI. Certain contributions to a retirement plan at work and to a traditional IRA may also reduce taxable income.

Marketplace Insurance

If changes to income, Medicare begins or changes to members of the family occurs make sure to notify the Marketplace to avoid having to pay back the advanced money. Also, if one gets married in the tax year this could also impact the Marketplace subsidy.

Issue 11: IRS Announces Extension of Free File Program Through 2029

The Internal Revenue Service announced an extension of the current Free File program through 2029 following an agreement that will continue to make the free private-sector tax software available to taxpayers.

The five-year extension agreement between the IRS and Free File Inc. will continue the program through October 2029.

Free File is a public-private partnership between the IRS and several tax preparation software companies who provide their online tax preparation and filing software for free. Through this partnership, tax preparation and filing software providers make their online products available to eligible taxpayers. The program is only available on IRS.gov.

This year, Free File saw an increase of about 200,000 tax returns filed through the program, reaching 2.9 million returns as of May 11. That’s an increase of 7.3% from the 2.7 million filed through the same period last year.

Now in its 22nd filing season, taxpayers across the nation can access free software products provided by IRS Free File trusted partners by visiting IRS.gov. Through this public-private partnership, tax preparation and filing software providers make their online products available to eligible taxpayers. Eight private-sector Free File partners provide online guided tax software products this year to any taxpayer with an Adjusted Gross Income (AGI) of $79,000 or less in 2023. In addition, those with an AGI over $79,000 can use the IRS’s Free File Fillable Forms. Free access to online products is only available by starting from IRS Free File.

The IRS noted that Free File remains available on IRS.gov for taxpayers through the Oct. 15 extension deadline for 2023 tax returns.

For 2024, partners participating in IRS Free File are:

- 1040Now

- Drake (1040.com)

- ezTaxReturn.com

- FileYourTaxes.com

- On-Line Taxes

- TaxAct

- TaxHawk (FreeTaxUSA)

- TaxSlayer

The IRS also saw interest this tax season in the Direct File pilot, which allowed taxpayers to file electronically directly with the IRS for the first time. Several hundred thousand taxpayers across 12 states signed up for Direct File accounts, and 140,803 taxpayers filed their federal tax returns using the new service.

The IRS also saw increased activity in free tax returns at Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE) sites, with 2.6 million returns prepared representing 200,000 more than a year ago.

Issue 12: IR-2024-148 – U.S. Taxpayers Living and Working Abroad Face June 17 Deadline to File their 2023 Tax Returns

The Internal Revenue Service reminds taxpayers living and working outside the United States to file their 2023 federal income tax return by Monday, June 17.

This deadline applies to both U.S. citizens and resident aliens abroad, including those with dual citizenship.

Qualifying for the June 17 extension

U.S. citizens or resident aliens residing overseas or on duty in the military outside the U.S. are allowed an automatic two-month extension to file their tax return and pay any amount due. A taxpayer qualifies for the June 17 extension to file and pay if:

- They are living outside of the United States and Puerto Rico and their main place of business or post of duty is outside the United States and Puerto Rico, or

- They are serving in the military outside the U.S. and Puerto Rico on the regular due date of their tax return.

To use the automatic two-month extension, taxpayers must attach a statement to their tax return explaining which of the two situations listed earlier applies.

Additional extensions

As a reminder, an extension of time to file a return does not grant an extension of time to pay taxes owed. Eligible taxpayers should estimate and pay any owed taxes by the June 17 deadline.

- Taxpayers who can’t meet the June 17 due date can request an automatic six-month extension by filing Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return.

- Taxpayers who need an extension of more than six months to meet either the bona fide residence or the physical presence test to qualify for the foreign earned income exclusion or to exclude or deduct the foreign housing costs must file IRS Form 2350, Application for Extension of Time to File U.S. Income Tax Return.

- Businesses that need more time must file Form 7004, Application for Automatic Extension of Time to File Certain Business Income Tax, Information and Other Returns.

- Members of the military stationed abroad or in a combat zone during tax filing season may qualify for an additional extension of at least 180 days to file and pay taxes. More information can be found in the Extension of Deadline – Combat Zone Service Q&As.

- Spouses of individuals who served in a combat zone or contingency operation are generally entitled to the same deadline extensions with some exceptions. Extension details and more military tax information is available in IRS Publication 3, Armed Forces’ Tax Guide.

The IRS encourages anyone needing additional time to file an extension electronically. Filers may use IRS Free File, regardless of income, to request an automatic extension of time to file, or choose from several options at IRS.gov/Extensions.

File to claim benefits.

Many taxpayers living outside the U.S. qualify for tax benefits, such as the Foreign Earned Income Exclusion and the Foreign Tax Credit, but they are available only if a U.S. return is filed.

In addition, the IRS encourages families to check out expanded tax benefits such as the Child Tax Credit, Credit for Other Dependents and Credit for Child and Dependent Care expenses, and claim them if they qualify. Though taxpayers abroad often qualify, the calculation of these credits differs depending upon whether they lived in the U.S. for more than half of 2023. For more information, see the instructions to Schedule 8812, Credits for Qualifying Children and Other Dependents, and the instructions to Form 2441, Child and Dependent Care Expenses.

Reporting required for foreign accounts and assets.

U.S. citizens or resident aliens’ world-wide income is generally subject to U.S. income tax, including income from foreign trusts and foreign bank and securities accounts. In most cases, affected taxpayers need to complete and attach Schedule B, Interest and Ordinary Dividends, to their Form 1040 series tax return. Part III of Schedule B asks about the existence of foreign accounts such as bank and securities accounts and usually requires U.S. citizens to report the country in which each account is located.

In addition, certain taxpayers may also have to complete and attach to their return Form 8938, Statement of Specified Foreign Financial Assets. Generally, U.S. citizens, resident aliens and certain nonresident aliens must report specified foreign financial assets on this form if the aggregate value of those assets exceeds certain thresholds. For details, see the instructions for this form.

Further, separate from reporting specified foreign financial assets on a tax return, certain foreign financial accounts, such as bank accounts or brokerage accounts, must be reported by electronically filing Form 114, Report of Foreign Bank and Financial Accounts (FBAR), with the Treasury Department’s Financial Crimes Enforcement Network (FinCEN). The FBAR requirement applies to U.S. persons with an interest in, or signature or other authority over foreign financial accounts whose aggregate value exceeded $10,000 at any time during 2023.

The IRS encourages U.S. persons with foreign assets, even relatively small ones, to check if this filing requirement applies to them. The form is available only through the Bank Secrecy Act E-Filing System. The deadline for filing the annual FBAR is April 15, 2024. However, FinCEN grants those who missed the April deadline an automatic extension until Oct. 15, 2024. There’s no need to request this extension. See FinCEN’s website for further information.

Report in U.S. dollars.

Any income received or deductible expenses paid in foreign currency must be reported on a U.S. tax return in U.S. dollars. Likewise, any tax payments must be made in U.S. dollars.

IRS Form 8938 requires the use of a Dec. 31 exchange rate for all transactions, regardless of the actual exchange rate on the date of the transaction. Generally, the IRS accepts any posted exchange rate that is used consistently. For more information on exchange rates, see Foreign Currency and Currency Exchange Rates.

The instructions for FinCEN Form 114 state that for accounts with non-United States currency, a filer should convert the maximum account value into United States dollars by using the U.S. Treasury Department’s Bureau of the Fiscal Service’s exchange rates as of the last day of the calendar year at issue. If no Bureau of the Fiscal Service rate is available, a filer can use another verifiable foreign currency exchange rate.

Making tax payments

To ensure tax payments are credited promptly, the IRS urges taxpayers to consider the convenience of paying their U.S. tax obligations electronically. The fastest and easiest way to do that is via their IRS Online Account, IRS Direct Pay and the Electronic Federal Tax Payment System (EFTPS). These and other electronic payment options are available at IRS.gov/Payments.

Reporting for expatriates

Taxpayers who relinquished their U.S. citizenship or ceased to be lawful permanent residents of the U.S. during 2023 must file a dual-status tax return and attach Form 8854, Initial and Annual Expatriation Statement. A copy of Form 8854 must also be filed with the IRS by the due date of the tax return (including extensions). See the instructions for this form and Notice 2009-85, Guidance for Expatriates Under Section 877A, for further

Issue 13: Summer Activities that Could Affect People’s Tax Returns in 2024

While summer is a time for fun, it’s never the wrong time to think about taxes – and some of those summer activities could have an impact. Here are a few summertime activities and tips on how taxpayers should consider them for filing season.

Marriage

Wedding season is upon us, and newlyweds can make their tax filing easier by taking two simple steps now:

- First, report any name change to the Social Security Administration.

- Next, notify the United States Postal Service, employers and the IRS of any address change. To officially change their mailing address with the IRS, taxpayers must compete and submit Form 8822, Change of Address. See page 2 of the form for detailed instructions.

- Finally, do not forget to notify the Marketplace of the marriage if one or both have insurance through the Marketplace. A marriage could affect their monthly payment. This could avoid a surprise during tax season of having to pay an amount back.

Summer camp

If a taxpayer is sending a child to summer camp, the cost may count toward the Child and Dependent Care Credit.

Business travel

Kids may have the summer off, but parents generally don’t – and business travel happens year-round. Tax deductions are available for certain people who travel away from their home or main place of work for business reasons. Whether a business traveler is away for a few nights or all summer long, it’s important for them to remember the tax rules related to business travel.

Part-time work

While summertime and part-time workers may not earn enough to owe federal income tax, they should file a tax return to get any refund they may be owed. Part-time and seasonal workers can visit IRS.gov to learn more about who should file a tax return.

Some taxpayers earn summer income with a side hustle or doing gig work. They can visit the Gig Economy Tax Center at IRS.gov to learn how participating in the gig economy can affect their taxes. If taxpayers are paid through payment apps for goods and services during the year, they may receive an IRS Form 1099-K for those transactions. For more information, go to IRS.gov/1099k.

Home improvements

The IRS has information to help taxpayers take advantage of potential tax benefits for home improvements. If taxpayers make qualified energy efficient improvements to their home after Jan. 1, 2023, they may qualify for a tax credit up to $3,200. They can claim the credit for improvements made through 2032.

These types of improvements include Energy Efficient Home Improvement Credits for things like water heaters, exterior windows and doors and heating and air conditioning installations. Residential Clean Energy Credits are available for taxpayers who install solar water heaters, fuel cells and battery storage or solar, wind and geothermal power generation. Taxpayers can visit the Home Energy Tax Credits page on IRS.gov to learn more.

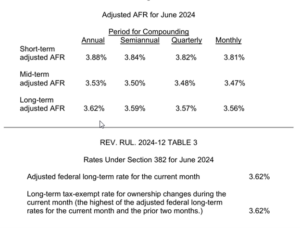

Issue 14: Applicable Federal Rates for June 2024, Rev. Rul. 2024-12

REV. RUL. 2024-12 TABLE 5

Rate Under Section 7520 for June 2024 4 Applicable federal rate for determining the present value of an annuity, an interest for life or a term of years, or a remainder or reversionary interest 5.6%

![]() Basics & Beyond Resources

Basics & Beyond Resources

- Blog Page

- Resource List

- Webinar & Seminar Schedules

- Get Registered!

- Note: Paid attendees can request a link to the replay of any previously recorded webinar presentations by emailing us at [email protected]