In this Issue:

(Note: Click on the Issue (link) to navigate directly to the newsletter section & Click on a “logo”–> ![]() to navigate back to the Top of the page.)

to navigate back to the Top of the page.)

We’re excited to introduce JoJo, the newest member of the Basics & Beyond customer support team — powered by AI and ready to make your life easier.

JoJo brings the power of automation and 30+ years of tax education expertise to your fingertips. As our AI customer support agent, JoJo is here to streamline your support experience and provide expert-level assistance, 24/7.

JoJo can assist you in seconds with a wide variety of support tasks, including:

✩ Retrieving your GoTo Webinar join or registration links

✩ Checking which Beyond & Basics sessions you’re registered for

✩ Accessing webinar playbacks (VODs) for sessions you’ve purchased

✩ Verifying state CPA requirements

✩ Submitting group registrations

✩ Sending messages to our support team

✩ Answering FAQs about Beyond & Basics policies and online resources

But that’s not all. JoJo also taps into our extensive content library to deliver deeper value to our community of tax professionals:

✩ Customer Service Questions: Need help navigating our site or resolving account issues? JoJo’s got you covered.

✩ Newsletter Archives: Quickly locate past articles from our acclaimed newsletter for expert guidance on evolving tax topics.

✩ Q&A Access from Webinars and Seminars: JoJo can retrieve previous questions and answers shared during our live events.

✩ Exploring General Tax Topics: From tax law changes to industry best practices discussed in our online sessions, JoJo offers tailored support for our attendees.

✩ Fast & Friendly: Get the information you need instantly, with no wait times.

✩ Expert-Backed: JoJo is powered by AI through decades of Basics & Beyond’s knowledge base and industry insights.

✩ Always Available: Whether it’s after hours or a weekend, JoJo is ready to assist.

✩ Personalized Support: Designed with tax professionals in mind, JoJo delivers relevant and specific attendee help.

Basics & Beyond has served the tax professional community for more than 30 years, offering trusted seminars, webinars, and resources. With JoJo, we’re bringing that legacy into the future by combining innovative AI with a deep knowledge base to support your success.

JoJo is live and ready to help! Click on JoJo in the lower right corner of the screen and start a conversation to see how JoJo can enhance your Basics & Beyond experience. From registration help to tax accreditation insights, JoJo is your always-on assistant for smarter support.

Consistent with the U.S. Department of the Treasury’s March 2, 2025 announcement, the Financial Crimes Enforcement Network (FinCEN) is issuing an interim final rule that removes the requirement for U.S. companies and U.S. persons to report beneficial ownership information (BOI) to FinCEN under the Corporate Transparency Act.

In that interim final rule, FinCEN revises the definition of “reporting company” in its implementing regulations to mean only those entities that are formed under the law of a foreign country and that have registered to do business in any U.S. State or Tribal jurisdiction by the filing of a document with a secretary of state or similar office (formerly known as “foreign reporting companies”). FinCEN also exempts entities previously known as “domestic reporting companies” from BOI reporting requirements.

Thus, through this interim final rule, all entities created in the United States — including those previously known as “domestic reporting companies” — and their beneficial owners will be exempt from the requirement to report BOI to FinCEN. Foreign entities that meet the new definition of a “reporting company” and do not qualify for an exemption from the reporting requirements must report their BOI to FinCEN under new deadlines, detailed below. These foreign entities, however, will not be required to report any U.S. persons as beneficial owners, and U.S. persons will not be required to report BOI with respect to any such entity for which they are a beneficial owner.

Statement from Acting Commissioner Dudek about Temporary Restraining Order Related to the Social Security Administration

“Today, the Court issued clarifying guidance about the Temporary Restraining Order (TRO) related to DOGE employees and DOGE activities at the Social Security Administration (SSA). Therefore, I am not shutting down the agency. President Trump supports keeping Social Security offices open and getting the right check to the right person at the right time. SSA employees and their work will continue under the TRO.”

Reports Say IRS Plans to Cut Staff by Half

Numerous media outlets report that the IRS is drafting plans to cut its workforce by as much as half through layoffs, attrition and incentivized buyouts. The IRS employs roughly 90,000 people nationwide, not including the 7,000 probationary employees laid off in February. A U.S. Office of Management and Budget memo sent to federal agencies in February said agency heads must prepare to initiate large-scale reductions in force no later than March 13.

DOGE Cancels Leases on 61 IRS Offices

The Department of Government Efficiency (DOGE) terminated the leases for 61 IRS offices nationwide, according to a list of terminated leases under the Real Estate heading on the department’s website. The lease terminations follow reports that the IRS will close more than 100 taxpayer assistance centers across the country as part of DOGE’s efforts to cut government waste. The IRS has previously reported that its taxpayer assistance centers helped 648,000 taxpayers in 2024.

| Alabama | Birmingham and Montgomery |

| Arizona | Glendale, Mesa and Phoenix |

| California | ElCentra, Modesto, San Marcos, Stockton, and Visalia and Thousand Oaks |

| Florida | Sarasota |

| Georgia | Macon and Savannah |

| Hawaii | Wailuku and Hilo |

| Iowa | Cedar Rapids and Sioux City |

| Idaho | Idaho Falls |

| Illinois | Champaign and Quincy |

| Kansas | Salina |

| Kentucky | Bowling Green, Hopkinsville, Owensboro and Paducah |

| Massachusetts | Lowell, Southborough, Springfield and Worcester |

| Maryland | Fredrick |

| Michigan | Marquette |

| Minnesota | Bloomington and St Cloud |

| Missouri | Jefferson City |

| Mississippi | Oxford and Columbus |

| North Carolina | Fayetteville and Wilmington |

| Nebraska | Scottsbluff |

| New York | New Windsor |

| Ohio | Mansfield and Cleveland |

| Oregon | Bend, Medford and Salem |

| Pennsylvania | Altoona and Erie |

| Puerto Rico | Guaynabo and Mayaguez |

| Tennessee | Chattanooga, Franklin* and Knoxville |

| Texas | Beaumont |

| Virginia | Fredericksburg and Roanoke |

| Vermont | Brattleboro |

| Wisconsin | La Crosse |

| West Virginia | Parkersburg |

*Frankin, TN has been closed

Treasury Ordered to Rehire Fired Employees

The U.S. Court of Appeals for the 9th Circuit upheld a district court order to reinstate probationary federal employees who were terminated in February. On March 13, a California federal district court judge ordered those 15,499 probationary federal employees, including 7,613 Treasury Department employees, be rehired.

After the district court’s ruling, the U.S. Office of Personnel Management filed an emergency motion with the 9th Circuit to pause the district court order to rehire the employees. The 9th Circuit found that rehiring the employees maintained the status quo while the lower court heard a challenge to the terminations brought by unions representing federal employees.

The Social Security Administration (SSA) announced the immediate resumption of debt collection activities through the Treasury Offset Program (TOP) for debts accrued prior to March 2020. This decision comes after a suspension of collections due to the economic challenges posed by the COVID-19 pandemic.

The Treasury Offset Program, administered by the Department of the Treasury’s Bureau of Fiscal Service, is a centralized program designed to collect delinquent debts owed to federal and state agencies by intercepting Federal and state payments. Since 1992, SSA has referred delinquent Old-Age, Survivors, and Disability Insurance (OASDI) and Supplemental Security Income (SSI) debts to TOP as mandated by law.

The Department of Treasury has begun collecting debts SSA referred to Treasury before March 2020, impacting an estimated 280,000 individuals with a collective debt balance of $2.7 billion.

As of March 27, the agency will begin mailing notices about the new 100% withholding rate, rather than the recent adjustment of just 10 %. The withholding rate change applies to new overpayments related to Social Security benefits. The withholding rate for current beneficiaries with an overpayment before March 27 will not change and no action is required. The withholding rate for Supplemental Security Income overpayments remains 10 %.

People who are overpaid after March 27 will automatically be placed in full recovery at a rate of 100 percent of the Social Security payment. If someone cannot afford full recovery of their overpayment, they can contact Social Security at 1-800-772-1213 or their local office to request a lower rate of recovery.

Additionally, people have the right to appeal the overpayment decision or the amount. They can ask Social Security to waive collection of the overpayment, if they believe it was not their fault and cannot afford to pay it back. The agency does not pursue recoveries while an initial appeal or waiver is pending.

The Social Security Administration (SSA) will no longer allow individuals to start their claims for benefits by telephone as of March 31. The change was announced in a press release explaining that the SSA is beginning a two-week transition plan to implement stronger identity verification procedures. When the transition period concludes on March 31, individuals seeking to claim benefits without using “my Social Security” online account can start their claim by telephone. The claim will not be completed until their identity has been verified in person at their local SSA office.

Individuals who want to change the direct deposit of their benefits will also be required to either use my Social Security or visit their local SSA office. However, the agency will also be expediting the processing of direct deposit change requests so that they are completed in one business day using the Treasury Department’s Account Verification Service (AVS). Prior to the change, changes to online direct deposits were held for 30 days.

Social Security Increases Transparency and Accountability

Shares More Information Online

The Social Security Administration (SSA) announced today several new initiatives and resources to promote greater transparency and accountability.

What to Know about Proving Your Identity: SSA recently announced it is strengthening identity proofing requirements for people who do not use a personal my Social Security account to apply for cash benefits or to change direct deposit information for benefits. To help the public understand the new policy, SSA today published a new webpage, What to Know about Proving Your Identity | SSA.

Weekly Operational Report Meetings: Acting Commissioner Dudek meets with his senior leadership team throughout the week to tackle a range of challenges facing the agency. During the Weekly Operational Report (WOR) meeting, leaders focus on specific topics, the options presented to the acting commissioner, and the resulting decisions made during these meetings.

Agency Actions: Acting Commissioner Dudek also published online a summary of select agency challenges, options presented, and the Acting Commissioner’s ultimate decisions. SSA plans to update this page periodically to include notable matters the current Administration is solving. Agency Actions | SSA

National 800 Number Wait Times: The American people do not receive the prompt customer service they deserve when calling the agency’s 800 number. Despite the knowledge, dedication, and experience of SSA’s telephone representatives, customers wait too long to speak with a representative. People deserve to know the wait time challenges they will face if unable to use the agency’s secure and convenient online services. Acting Commissioner Dudek is increasing the level of detail shared with the public to provide an honest and transparent view of wait times.

Efficiencies and Cost Avoidance: SSA works closely with the General Services Administration to identify unused and underutilized office space. SSA published its Efficiencies and Cost Avoidance webpage that lists soft-term lease terminations, including an explanation for each location and whether any change affects the public or not. For nearly all locations, the space being terminated is only a small room within the larger Social Security office location.

Workforce Update: SSA identified opportunities to optimize its workforce by offering voluntary opportunities to depart the agency or move to a front-line customer service position. More on buyouts further in the newsletter.

Social Security announced today that more than three million deaths are reported to the Social Security Administration each year and explains that the agency’s records are highly accurate. Of these millions of death reports received each year, less than one-third of 1 % are erroneously reported deaths that need to be corrected.

Deaths are reported to Social Security primarily from the States, but also from other sources, including family members, funeral homes, Federal agencies, and financial institutions. In a 2008 audit report, the IG noted that “SSA receives most death reports from funeral homes or friends/relatives of the deceased. SSA considers such first party death reports to be verified and immediately posts them to the Death Master File.”

If a person suspects that they have been incorrectly listed as deceased on their Social Security record, they should contact their local Social Security office as soon as possible. They can locate their nearest Social Security office at www.ssa.gov/agency/contact/. They should be prepared to bring at least one piece of current (not expired) original form of identification. Social Security takes immediate action to correct its records, and the agency can provide a letter that the error has been corrected that can be shared with other organizations, agencies, and employers.

Funeral homes generally tell the Social Security Administration when someone dies. If a funeral home is not involved or does not report the death for some reason, you should call us and provide the name, Social Security number, date of birth, and date of death for the person who died.

Call +1 800-772-1213

Outside the United States – If you live outside the United States, contact a Federal Benefits Unit. If the person who died was a U.S. citizen, you should also report the death to the nearest U.S. embassy or consulate.

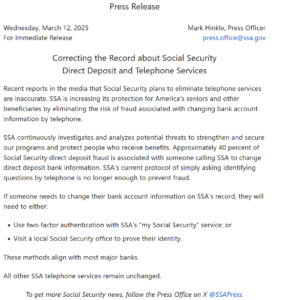

Recent reports in the media say that Social Security plans to eliminate telephone services are inaccurate. SSA is increasing its protection for America’s seniors and other beneficiaries by eliminating the risk of fraud associated with changing bank account information by telephone.

SSA continuously investigates and analyzes potential threats to strengthen and secure our programs and protect people who receive benefits. Approximately 40 % of Social Security direct deposit fraud is associated with someone calling SSA to change direct deposit bank information. SSA’s current protocol of simply asking identifying questions by telephone is no longer enough to prevent fraud.

If someone needs to change their bank account information on SSA’s record, they will need to either:

These methods align with most major banks.

All other SSA telephone services remain unchanged.

The Social Security Administration (SSA) is sharing its significant progress in identifying and correcting beneficiary records of people 100 years old or older. The data reported in the media represent people who do not have a date of death associated with their record. While these people may not be receiving benefits, it is important for the agency to maintain accurate and complete records.

The agency follows long established program integrity initiatives that identify people who have a higher likelihood of being deceased due to their age or incomplete death reports. For example, SSA receives data from the Centers for Medicare and Medicaid Services of individuals who have not used Medicare Part A or Part B for three or more years. SSA uses the data as an indicator to select and prioritize cases of individuals aged 90 or older, who are currently in pay status and living in the United States, to determine continued eligibility for Social Security benefits. The agency attempts to conduct an interview with these individuals to verify they are still alive. If the agency identifies someone who is deceased, it immediately stops payment and reports any suspicions of fraud to SSA’s Office of the Inspector General.

The Social Security Administration (SSA) is sharing its significant progress to quickly implement the Social Security Fairness Act. Through March 4, 2025, SSA has already paid 1,127,723 people more than $7.5 billion in retroactive payments. The retroactive payments are the result of the repeal of the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO). The average retroactive payment so far is $6,710.

The WEP and GPO provisions reduced or eliminated the Social Security benefits for over 3.2 million people who receive a pension based on work that was not covered by Social Security (a “non-covered pension”) because they did not pay Social Security taxes.

The agency continues to pay remaining retroactive payments and is ready to begin paying higher monthly benefit payments beginning in April for people’s March benefit.

The following message was sent to agency employees:

The Social Security Administration (SSA) will soon implement agency-wide organizational restructuring that will include significant workforce reductions. Through these massive reorganizations, offices that perform functions not mandated by statute may be prioritized for reduction-in-force actions that could include abolishment of organizations and positions, directed reassignments, and reductions in staffing. The agency may reassign employees from non-mission critical positions to mission critical direct service positions (e.g., field offices, teleservice centers, processing centers). Reassignments may be involuntary and may require retraining for new workloads.

VOLUNTARY REASSIGNMENTS

Employees interested in voluntarily being reassigned to a mission critical position should indicate their interest with the Reassignment Questionnaire by March 14, 2025.

VOLUNTARY SEPARATION INCENTIVES

Employees who do not wish to undergo the restructuring process may elect to separate from federal service through retirement or resignation. To further support employees considering these options, SSA is offering the following to ALL EMPLOYEES:

VOLUNTARY EARLY RETIREMENT (VERA) OR “EARLY OUT”

VOLUNTARY SEPARATION INCENTIVE PAYMENTS (VSIP)

Up to GS 8 | $15,000 |

GS 9 – 12 | $20,000 |

GS 13 and up | $25,000 |

OPTIONAL RETIREMENT

Employees who have reached their full retirement age may apply for optional retirement at any time. Employees serving under the Federal Employees Retirement System (FERS) should see the OPM eligibility information for FERS, which is generally 30 years of service, plus reaching minimum retirement age. Employees serving under the Civil Service Retirement System (CSRS) should refer to the OPM eligibility information for CSRS, which is generally 30 years of service and age 55. Additional provisions and options are available for both FERS and CSRS.

RESIGNATION

Employees may resign from federal service at any time. Employees who resign would be eligible for a payout of their annual leave and may be eligible to apply for a Deferred Retirement when they reach their minimum retirement age. Please see the attached table explaining the differences between resignations and retirements and the benefits that would apply.

Mistakes can happen when preparing a tax return – and that can cause delays or even rejected returns. Knowing what to lookout for can help you be better prepared when filing federal tax return.

Electronically filing a tax return reduces errors because the tax software does the math, flags common errors and prompts for missing information.

Common errors:

Here are some common errors to avoid:

The Internal Revenue Service is making it easier for taxpayers to file their taxes by adding information return documents to their IRS Individual Online Account, helping consolidate important tax records into one digital location.

The first information returns to be added are Form W-2, Wage and Tax Statement and Form 1095-A, Health Insurance Marketplace Statement. These forms will be available for tax years 2023 and 2024 under the Records and Status tab in the taxpayer’s Online Account.

Only information return documents issued in the taxpayer’s name will be available in their Online Account. Their spouse must log into their own Online Account to retrieve their information return documents. This is true whether they file a joint or separate return. Importantly, state and local tax information, including state and local tax information on Form W-2, will not be available on Individual Online Account. Filers should continue to keep the records mailed to them by the original reporter.

Create an IRS Individual Online Account

Individuals can create or access their Online Account on IRS.gov at Online Account for Individuals. In addition to Forms W-2 and 1095-A, people can:

The IRS continues to expand its online capabilities with the Business Tax Account tool, giving a growing number of eligible business taxpayers a quicker and easier way to access tax information online and meet their tax obligations.

Sole proprietors, individual partners of partnerships, individual shareholders of S corporations and C corporations should check if they are eligible to use Business Tax Account.

Features and tools of BTA

Features and access depend on the business structure and the individual’s role in the business. Business taxpayers can make electronic payments, set up a future payment or cancel a scheduled payment. They can also access:

For more on the most recent updates on BTA, check out the December 2024 Fact Sheet on Business Tax Account.

The IRS released the adjusted the 2025 limitations on housing expenses for §911 in IRS Notice 2025-16. Qualified taxpayers can exclude foreign-earned income up to a certain amount ($130,000 for the year 2025) and deduct or exclude eligible housing costs under §911(c), subject to certain limitations. The geographic differences and the varying housing costs throughout the United States determine adjustments. If you have a client who works overseas, review their income and housing expenses to determine if they are eligible to apply the 2025 higher limitations to their 2024 tax returns.

The Justice Department filed a civil injunction suit to permanently bar tax return preparer Juan Humberto Garcia, his son-in-law Marcos Yariel Figueroa, and Garcia’s business, from preparing federal tax returns for others. The complaint alleges the two prepared false federal tax returns through Tax Master. The IRS interviewed Tax Master customers who said they did not give Garcia or Figueroa any reason to believe that the items reported on their returns were legitimate. By repeatedly understating their customers’ tax liabilities, the preparers at Tax Master have caused the United States to lose substantial tax revenue. The complaint asks the court to order the defendants to turn over the ill-gotten tax preparation fees.

A federal court in Louisiana, convicted Whylithia R. Robinson in contempt for violating a permanent injunction that forbade her and her business from preparing, filing, or assisting in the preparation or filing of federal tax returns for others. In January 2023, the United States filed a complaint against Robinson and AAA Tax Service. The complaint alleges from 2019-2021, Robinson prepared and filed 2,629 fraudulent income tax returns. In April 2023, the court issued a default judgment of permanent injunction that barred Robinson and AAA Tax Services from preparing tax returns. Following a hearing last week, the court found that Robinson violated the permanent injunction by continuing to prepare tax returns for others. The court found Robinson in civil contempt and mandated that she reimburses the United States for its costs of litigation and travel expenses.

Extending the Trump Tax Cuts

Restoring and extending the 2017 Trump tax cuts will fuel significant economic growth and prosperity.

Key Policies from the Trump Tax Cuts Set to Expire if Congress Fails to Act:

Over the next 10 years, small businesses will increase GDP by $75 billion each year because of the 20 % small business deduction, and then rise to $150 billion every year after, according to a study released by the National Federation of Independent Businesses.

These figures represent new small businesses, new facilities, and new workers if the 20 % small business deduction is extended. The growth generated by extending the Trump tax cuts would also result in small businesses creating an additional 1 million jobs every year over the next decade and an additional 2 million jobs in the years that follow with the continuation of the policy.

COVID Unemployment Fraud

Sixteen days before the statute of limitations to prosecute the theft of COVID-era unemployment insurance (UI) fraud expires, the U.S. House of Representatives with bipartisan support, voted to extend the deadline from five years to ten years to ensure criminals that stole UI benefits are brought to justice and to recover billions in taxpayer dollars.

The legislation, the Pandemic Unemployment Fraud Enforcement Act, helps fulfill President Trump’s mandate to recover taxpayer money lost to waste, fraud, and abuse. Government estimates show between $100 to $135 billion in UI benefits were stolen by fraudsters, gang members, prisoners, international crime rings, and hackers from Nigeria during the pandemic. Other estimates peg the total amount of taxpayer dollars stolen at $400 billion. Of that, only $5 billion has been recovered so far.

The statute of limitations for prosecuting pandemic unemployment benefits starts to expire on March 27, jeopardizing ongoing prosecutions and future efforts to pursue these criminals. According to the Department of Labor and Department of Justice, there are over 157,000 open UI fraud hotline complaints and more than 1,648 open, uncharged COVID-19 fraud investigations. The bill allows law enforcement to prosecute these and new cases on behalf of taxpayers.

When the Ways and Means Committee considered the legislation earlier this year, every single committee Democrat voted against the bill. However, on the House floor 83 Democrats voted in favor of the bill.

Pandemic Unemployment Fraud Enforcement Act (H.R. 1156)

Extends the statute of limitations for prosecuting COVID-era unemployment insurance fraud from five to 10 years.

In 2022, Congress similarly extended the statute of limitations for prosecuting fraud in the Paycheck Protection Program and Economic Injury and Disaster Loans to 10 years.

House Passes Ways & Means Legislation to Rollback Biden Administration’s Midnight Crypto Rule in Bipartisan Vote

The House of Representatives voted overwhelmingly to rollback a last-minute cryptocurrency rule published by the Department of Treasury in the waning days of the Biden Administration that would cripple American digital asset leadership, stifle innovation, and burden American entrepreneurs. H.J.Res.25, introduced by Ways and Means member Representative Mike Carey (OH-15), repeals the Internal Revenue Service’s (IRS) “DeFi Broker Rule” which would devastate the American digital asset industry and American innovation by requiring those participating on decentralized finance exchanges to satisfy unworkable and overly burdensome reporting requirements – including collecting sensitive taxpayer information. According to IRS estimates, the rule would produce at least 8 billion new pieces of paperwork for taxpayers to submit to the agency and for IRS employees to collect and analyze.

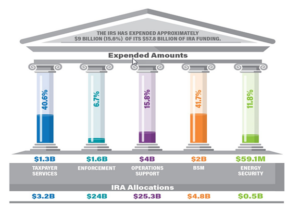

The IRS originally received $79.4 billion in supplemental funding when the President signed the Inflation Reduction Act of 2022 (IRA) into law in August 2022.

Congress subsequently rescinded approximately $21.6 billion in IRA funding, reducing the available IRA funding to approximately $57.8 billion. In addition to the rescissions, the American Relief Act, 2025, which provides appropriation funding to federal agencies through March 14, 2025, froze another $20.2 billion in IRA enforcement funds. This supplemental funding is available through Sept. 30, 2031.

Impact on Tax Administration

TIGTA initiated this review to provide periodic reporting on the IRS’s use and accounting for expenditures using IRA funding. This report provides a quarterly and cumulative snapshot of how the funding has been expended through Sept. 30, 2024. The IRS’s IRA supplemental funding is intended to help improve taxpayer services, modernize technology, and increase compliance and enforcement actions against high-income taxpayers and large corporations.

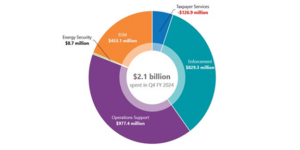

As of Sept. 30, 2024, the IRS has expended approximately $9 billion (15.6 %) of its $57.8 billion in IRA funding. In addition to the expended amounts shown in the graphic, the IRS expended approximately $11.6 million in Fiscal Year (FY) 2023 for the direct e-file tax return study, which is included in the total amount expended.

Of the $9 billion IRA funding expended as of Sept. 30, 2024, approximately $2.1 billion occurred in the fourth quarter of FY 2024. The negative amount in the Taxpayer Services funding activity reflects a realignment of obligations primarily to discretionary accounts as approved Information Technologies funds were available.

Full Report can be accessed here.

Quarterly Snapshot: The IRS’s Inflation Reduction Act Spending Through September 30, 2024

Taxpayers should make sure they have all their documents before filing a federal tax return. Those who haven’t received a W-2 or Form 1099 should contact the employer, payer or issuing agency and request the missing or corrected documents.

If a taxpayer does not receive the missing or corrected form in time to file their tax return, they can estimate the wages or payments made to them, as well as any taxes withheld. To avoid filing an incomplete return, they may need to use Form 4852, Substitute for Form W-2, Wage and Tax Statement, or Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, Etc.

If they receive the missing or corrected Form W-2 or Form 1099-R after filing their tax return and the information differs from their previous estimate, they must file Form 1040-X, Amended U.S. Individual Income Tax Return.

Most taxpayers should have received their documents by Jan. 31. These may include:

Incorrect Form 1099-G for unemployment benefits

Taxpayers must report unemployment compensation on their tax return as it is taxable income.

Taxpayer’s who receive an inaccurate Form 1099-G should contact the issuing state agency to request a revised Form 1099-G showing their correct benefits. Taxpayers who are unable to get a timely, corrected form from states should still file an accurate tax return, reporting only the income they did receive.

If the taxpayer did not receive unemployment benefits but did receive a Form 1099-G for unemployment compensation, this may be a sign that the taxpayer’s identity was stolen.

REV. RUL. 2025-8 TABLE 2

Basics & Beyond, Inc. is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State Boards of Accountancy have the final authority on the acceptance of individual course for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.nasbaregistry.org.