Stay informed with the November 2024 Tax Newsletter

![]() In this Issue:

In this Issue:

- Social Security Announces 5 % Benefit Increase for 2025

- IRS Invites Public Feedback on Draft Form 7217 Partner’s Report of Property Distributed by a Partnership

- IRS Direct File Set to Expand Availability in a Dozen New States and Cover Wider Range of Tax Situations for the 2025 Tax Filing Season

- IRS Accelerates Work on Employee Retention Credit Claims; Agency Currently Processing 400,000 Claims Worth About $10 billion

- IRS Shares Directions for Replying to ERC Disallowance Letter

- IRS Extends Relief to Farmers and Ranchers Impacted by Drought in 41 States, Other Regions

- IRS Releases 2022 Tax Gap Projections; Voluntary Compliance Rate Among Taxpayers Remains Steady

- Energy Credits Online Tool Helps Businesses Claim Credits

- Filing Information Returns Electronically (FIRE) System Automatic 30-Day Fill-in Extension of Time Requests Require a Transmitter Control Code (TCC)

- Treasury and IRS Issue Guidance for the Energy Efficient Home Improvement Credit

- IRS Announces Launch of Pass-through Compliance Unit in LB&I; New Group Brings Together Teams of Specialists from Across the Agency to Tackle Large or Complex Exams

- IRS Encourages all Taxpayers to Sign up for an IP PIN for the 2025 Tax Season

- IRS Releases Notices on Expenses Treated as Amounts Paid for Medical Care and Preventive Care for Purposes of Qualifying as an HDHP Under § 223

- Current PTINs Expire Dec. 31

- Applicable Federal Rates for November 2024, Rev. Rul. 2024 – 24

- What Are Mandatory 401(k) Roth Contributions Under the SECURE 2.0 Act?

***********************************************************************************************************************

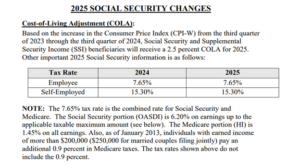

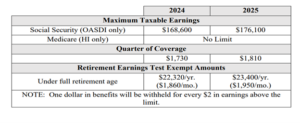

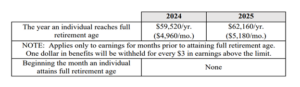

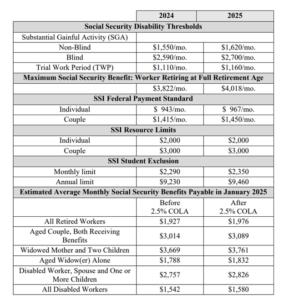

![]() Issue 1: Social Security Announces 2.5 % Benefit Increase for 2025

Issue 1: Social Security Announces 2.5 % Benefit Increase for 2025

Social Security Changes – COLA Fact Sheet (ssa.gov)

![]() Issue 2: IRS Invites Public Feedback on Draft Form 7217

Issue 2: IRS Invites Public Feedback on Draft Form 7217

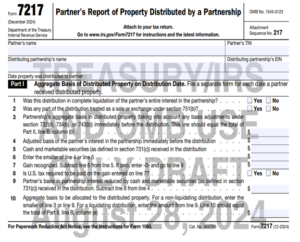

The IRS welcomes public feedback on draft Form 7217 and its accompanying instructions. On Aug. 28, the IRS released draft Form 7217, with the new title “Partner’s Report of Property Distributed by a Partnership.” The new tax form will be used for distributions to partners made in the 2024 tax year.

The form’s objective is to document every property distribution that a partner gets from a partnership. According to draft instructions posted by the IRS on Sept. 3, any partner receiving a property distribution from a partnership is required to file Form 7217.

The purpose of Form 7217 is to report all distribution of property that a partner receives from a partnership. A partner receiving a distribution of property from a partnership in a non-liquidating or liquidating distribution will use the form to report the basis of the distributed property.

In addition to disclosing the basis of distributed property, the new draft Form 7217 (Partner’s Report of Property Distributed by a Partnership) would also collect information about the inputs of the partner’s basis computation. The new form would not necessarily increase the amount of technical work required to compute basis for partners who receive property distributions. However, the draft Form 7217 represents another instance in an ongoing trend by the IRS to require more detailed information reporting by partnerships and partners.

§ 732 provides the rules for computing a partner’s basis in property distributed from a partnership to a partner. For a non-liquidating distribution, the partner’s basis in the property is equal to the partnership’s pre-distribution basis in the property but may not exceed the partner’s pre-distribution basis in its partnership interest (outside basis).

A partner’s basis in property received in a liquidating distribution is equal to the partner’s outside basis. For both current and liquidating distributions, the partner reduces the basis of its partnership interest first by the amount of money distributed to the partner (actual or deemed) in the same transaction.

§ 732 also provides rules to allocate basis across multiple properties distributed as part of the same transaction. While the distributing partnership must report certain information to the distributee partner to enable it to compute its basis in the distributed property, currently the distributee partner is not required to specifically report its basis computation of the distributed property to the IRS.

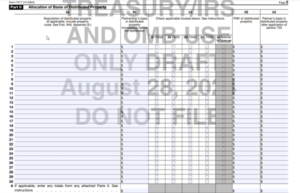

The draft Form 7217 would require a partner who receives a property distribution to disclose information about the distribution, such as whether it was in liquidation of the partner’s interest and whether § 751(b) applied to any part of the distribution.

The draft form then provides space for the partner to report the inputs for a § 732 computation on a property-by-property basis. Information required to be disclosed in the draft form includes:

- The partnership’s basis is in the property immediately prior to the distribution.

- The fair market value of the distributed property

- Whether the partner’s basis computation was impacted by special basis adjustments (e.g., §§ 743(b) or 734(b) adjustments) with respect to the property, and

- Finally, the partner’s basis in the distributed property after application of 732.

The draft Form 7217, if finalized, would be required for partners’ tax years beginning in 2024 or later. Because the form is still in the draft stage, taxpayers will need to watch for any revisions that are made when the form is finalized.

![]() Issue 3: IRS Direct File Set to Expand Availability in a Dozen New States and Cover Wider Range of Tax Situations for the 2025 Tax Filing Season

Issue 3: IRS Direct File Set to Expand Availability in a Dozen New States and Cover Wider Range of Tax Situations for the 2025 Tax Filing Season

The Internal Revenue Service announced that Direct File will be available for the 2025 tax filing season in double the number of states than last year’s pilot, and it will cover a wider range of tax situations, greatly expanding the number of taxpayers eligible to use the free e-filing service.

State and eligibility expansion

For the 2025 tax filing season, eligible taxpayers in 24 states will be able to use Direct File: 12 states that were part of the pilot last year, plus 12 new states where Direct File will be available in the upcoming filing season.

During the pilot last year, Direct File was available in Arizona, California, Florida, Massachusetts, Nevada, New Hampshire, New York, South Dakota, Tennessee, Texas, Washington State and Wyoming. For the 2025 tax filing season, Direct File will also be available in Alaska, Connecticut, Idaho, Kansas, Maine, Maryland, New Jersey, New Mexico, North Carolina, Oregon, Pennsylvania and Wisconsin.

In 2025, more than 30 million taxpayers in those 24 states will be eligible to use Direct File. Additional states could still join Direct File in 2025, and several states have expressed interest or announced that they will participate in Direct File in 2026.

In addition to doubling the number of states where Direct File will be available, the service will also cover a wider range of tax situations for the 2025 filing season.

During the pilot last year, Direct File covered limited tax situations, including wage income reported on a W-2 form, Social Security income, unemployment compensation and certain credits and deductions. For the 2025 filing season,

Direct File will support 1099’s interest income greater than $1,500, retirement income and 1099 for Alaska residents reporting the Alaska Permanent Fund dividend.

During the pilot, Direct File supported taxpayers claiming the Earned Income Tax Credit, Child Tax Credit and Credit for Other Dependents. This year, Direct File will also cover taxpayers claiming the Child and Dependent Care Credit, Premium Tax Credit, Credit for the Elderly and Disabled, and Retirement Savings Contribution Credits. In addition to covering taxpayers claiming the standard deduction and deductions for student loan interest and educator expenses, this year, Direct File will support taxpayers claiming deductions for Health Savings Accounts. Over the coming years, the IRS will gradually expand Direct File’s scope to support most common tax situations, focusing – in particular – on tax situations that impact working families.

![]() Issue 4: IRS Accelerates Work on Employee Retention Credit Claims; Agency Currently Processing 400,000 Claims Worth About $10 billion

Issue 4: IRS Accelerates Work on Employee Retention Credit Claims; Agency Currently Processing 400,000 Claims Worth About $10 billion

The Internal Revenue Service announced continued progress on Employee Retention Credit claims, with processing underway on about 400,000 claims, representing about $10 billion of eligible claims.

Work on the claims for small businesses and others is ongoing as the agency continues to navigate a large volume of claims from the complex pandemic-era credit. A significant number of the Employee Retention Credit (ERC) claims came in during a period of aggressive marketing by promoters, leading to a large percentage of improper, ineligible claims.

The approximately 400,000 claims being processed include eligible and ineligible claims, with the vast majority in this tranche being processed for approval. The total value of eligible claims represents about $10 billion. Checks are being mailed for eligible claims with refunds, with more planned in the weeks and months ahead.

New consolidated claim process for third-party payers helps with claims

To help speed processing, the IRS announced last month the opening of a consolidated claim process to help third-party payers and their clients resolve incorrect claims for the Employee Retention Credit.

Third-party payers report and pay clients’ federal employment taxes under the third-party payer’s Employer Identification Number. They handle clients’ payroll and tax reporting duties. Some of these TPPs filed ERC claims for multiple employers. If a third-party payer’s client has since determined it is ineligible for the ERC and wants to resolve their claim, it is the third-party payer that needs to correct it.

The consolidated claim process lets a third-party payer that filed a prior claim with multiple clients “withdraw” only some clients’ claims while maintaining the claims of the qualifying clients.

The ERC program began as an effort to help businesses during the pandemic, but as time went on the program increasingly became the target of aggressive marketing – and potentially predatory in some cases – well after the pandemic ended. Some promoter groups called the credit by another name, such as a grant, business stimulus payment, government relief or other names besides ERC or the Employee Retention Tax Credit (ERTC).

In addition to processing valid claims, the IRS is continuing to work denials of improper ERC claims, intensifying audits and pursuing civil and criminal investigations of potential fraud and abuse. The findings of the IRS review, announced in June, confirmed concerns raised by tax professionals and others that there was an extremely high rate of improper ERC claims in the current inventory of ERC claims.

Voluntary Disclosure Program remains open through Nov. 22; Withdrawal Program also available

The IRS reminds businesses that have received Employee Retention Credit payments to recheck eligibility requirements and consider the second Employee Retention Credit (ERC) Voluntary Disclosure Program (VDP) to resolve incorrect claims without penalties or interest.

The second ERC-Voluntary Disclosure Program will run through Nov. 22, 2024, and allow businesses to correct improper payments at a 15% discount and avoid future audits, penalties and interest.

The reopening of the ERC Voluntary Disclosure Program is designed to help businesses with questionable claims to self-correct and repay the credits they received after filing ERC claims in error. Many of these claims were driven by aggressive marketing from unscrupulous promoters.

As the IRS continues intensifying compliance work involving improper ERC claims, the VDP can protect businesses from potential costly compliance action in the future, such as audits, full repayment, penalties and interest. Full details are available in IRS Announcement 2024-30.

The IRS’s claim withdrawal program remains open for businesses whose ERC claims haven’t been paid yet.

![]() Issue 5: IRS Shares Directions for Replying to ERC Disallowance Letter

Issue 5: IRS Shares Directions for Replying to ERC Disallowance Letter

Businesses that claimed the Employee Retention Credit may have received IRS Letter 105-C if the IRS identified their claim as ineligible. Letter 105-C means the IRS disallowed, or denied, the Employee Retention Credit that a business claimed either as a refund or as a reduction of the tax owed for the tax period.

The Understanding Letter 105-C, Disallowance of the Employee Retention Credit page on IRS.gov can help businesses learn about next steps if they disagree with the disallowance. This new page has information on:

- Rechecking eligibility for the credit before disagreeing

- Responding to the letter, including what documentation to send the IRS

- Requesting an appeal or filing suit and the timelines to do so

![]() Issue 6: IRS Extends Relief to Farmers and Ranchers Impacted by Drought in 41 States, Other Regions

Issue 6: IRS Extends Relief to Farmers and Ranchers Impacted by Drought in 41 States, Other Regions

The Internal Revenue Service has announced guidance providing tax relief for farmers and ranchers in applicable regions forced to sell or exchange livestock because of drought conditions.

Under the guidance, farmers and ranchers may have an extended period of time to replace their livestock and defer tax on any gains from the forced sales or exchanges.

Notice 2024-70 provides a list of the applicable areas, by county or other jurisdiction, designated as eligible for federal assistance. The list includes 41 states and other regions for which drought was reported during the 12-month period ending on Aug. 31, 2024.

The tax relief generally applies to capital gains realized by eligible farmers and ranchers on sales or exchanges of livestock held for draft, dairy or breeding purposes. Sales of other livestock, such as those raised for slaughter or held for sporting purposes, or poultry, are not eligible.

The livestock sales or exchanges must be solely due to drought causing an area to be designated as eligible for federal assistance. Livestock generally must be replaced within a four-year period, instead of the usual two-year period. The IRS is authorized to further extend this replacement period if the drought continues.

The replacement period extension announced in the notice gives eligible farmers and ranchers four years until the end of their first tax year after the first drought-free year to replace the sold or exchanged livestock. As a result, eligible farmers and ranchers whose drought-sale replacement period was scheduled to expire at the end of 2024 will have until the end of their next tax year to replace the sold or exchanged livestock.

The IRS provides this extension to eligible farmers and ranchers if the applicable region is listed as suffering exceptional, extreme or severe drought conditions during any week between Sept. 1, 2023, and Aug. 31, 2024. This determination is made by the National Drought Mitigation Center.

Details, including an example of how this provision works, can be found in Notice 2006-82, available on IRS.gov.

![]() Issue 7: IRS Releases 2022 Tax Gap Projections; Voluntary Compliance Rate Among Taxpayers Remains Steady

Issue 7: IRS Releases 2022 Tax Gap Projections; Voluntary Compliance Rate Among Taxpayers Remains Steady

The Internal Revenue Service released the tax gap projections for tax year 2022, a detailed analysis showing the nation’s projected gross tax gap at $696 billion. This reflects the difference between projected ‘true’ tax liability and the amount of tax that is actually paid on time.

The new tax gap projections reflect an increase over the tax year 2014-2016 estimates and the tax year 2017-2019 projections. The 2022 projection is an increase of $200 billion over tax years 2014-2016.

However, the IRS noted that the increase for 2022 is similar to the 41% increase in the economy since the 2014-2016 time period as measured by the Gross Domestic Product. With the new study also showing the voluntary compliance rate among taxpayers remaining steady at 85%, the IRS noted the tax gap increase ultimately reflects growth in the economy and changes in the sources of income – not a change in taxpayer behavior involving filing or paying their taxes.

In addition, the new tax gap projections reflect the time period before the IRS began increasing tax compliance work following passage of the Inflation Reduction Act (IRA) in August of 2022. Since then, the IRS has stepped up compliance activity in a variety of areas with additional funding, including the agency collecting an initial $1.3 billion from high-income non-filers following IRA funding.

The new projections are published in Tax Gap Projections for Tax Years 2021 and 2022 (IRS Publication 5869).

Gross tax gap

The projected $696 billion gross tax gap is the difference between projected ‘true’ tax liability for a given period and the amount of tax that is paid on time. The gross tax gap covers three key areas – non-filing of taxes, underreporting of taxes and underpayment of taxes.

- Non-filing, which means tax not paid on time by those who do not file on time:

- $63 billion in tax year 2022, representing 9% of the gross tax gap.

- Underreporting, which reflects tax understated on timely filed returns.

- $539 billion in tax year 2022, representing 77% of the gross tax gap.

- Underpayment, or tax that was reported on time, but not paid on time.

- $94 billion in tax year 2022, representing 14% of the gross tax gap.

The primary focus on tax gap estimation is to measure compliance behavior as manifested in tax paid voluntarily and on time. The tax gap estimates and projections provide insight into the historical scale of tax compliance and to the persisting sources of low compliance.

After IRS compliance efforts and other late payments are factored in, the projected share of taxes eventually paid is 86.9% for tax year 2022, down slightly from the 87% for tax years 2014-2016.

![]() Issue 8: Energy Credits Online Tool Helps Businesses Claim Credits

Issue 8: Energy Credits Online Tool Helps Businesses Claim Credits

IRS Energy Credits Online, or IRS ECO, is a free electronic service that is secure, accurate and requires no special software.

Vehicle sellers and dealers can use the new IRS Energy Credits Online tool to register their business and complete time of sale reports online. Qualified manufacturers can use it to submit eligible clean vehicle VINs. Qualifying businesses, tax-exempt organizations or entities such as state, local and Indian tribal governments can register using this tool to take advantage of the elective payment or transfer of credits.

![]() Issue 9: Filing Information Returns Electronically (FIRE) System Automatic 30-Day Fill-in Extension of Time Requests Require a Transmitter Control Code (TCC)

Issue 9: Filing Information Returns Electronically (FIRE) System Automatic 30-Day Fill-in Extension of Time Requests Require a Transmitter Control Code (TCC)

To protect IRS systems, a transmitter control code (TCC) is now required to use the FIRE System automatic 30-day Fill-in extension of time. To use this option, you must complete an Information Returns (IR) Application for TCC, if you don’t already have a TCC. When completing your application, you will not see an option for the Fill-in extension of time. You simply need to select the form type for which you will be requesting the extension. For assistance, review Publication 5911, IR Application for TCC Tutorial, located on the FIRE page on IRS.gov.

Don’t wait, complete your application today to ensure you are ready for tax year 2024 filing season.

![]() Issue 10: IR-2024-280 – Treasury and IRS Issue Guidance for the Energy Efficient Home Improvement Credit

Issue 10: IR-2024-280 – Treasury and IRS Issue Guidance for the Energy Efficient Home Improvement Credit

Treasury and IRS issued Revenue Procedure 2024-31 and proposed regulations to provide guidance for the energy efficient home improvement credit.

The revenue procedure provides procedures and requirements that a manufacturer of specified property must follow to be treated as a qualified manufacturer (QM). To become a QM, a manufacturer must:

- Register and enter into an agreement with the IRS.

- Assign a qualified product identification number (PIN) unique to each item of specified property.

- Label such items with PINs.

- Make periodic reports to the IRS of PINs assigned.

Soon manufacturers will be able to use IRS Energy Credits Online Portal (IRS ECO) to register with the IRS. IRS ECO is a free electronic service that is secure and requires no special software, making it accessible to large and small businesses alike.

Taxpayers can use the IRS ECO platform to register and provide information to the IRS for filing purposes. In addition, IRS ECO incorporates validation checks and other risk-mitigation measures and allows for monitoring in real time of key metrics to include identification of customer-service enhancements and fraudulent activity.

For property placed in service beginning in 2023, a taxpayer may take credit equal to 30% of the total amount paid for certain energy efficient products or for a home energy audit.

The credit is limited to certain amounts, per taxpayer and per tax year. A taxpayer may claim a total credit of up to $3,200, with a general total limit of $1,200, and a separate total limit of $2,000 for electric or natural gas heat pump water heaters, electric or natural gas heat pumps, and biomass stoves or boilers that meet certain requirements.

The $1,200 general limit also includes additional limitations specific to certain types of property that meet the requirements:

- $600 for any item of qualified energy property.

- $600 in total for exterior windows and skylights.

- $250 for an exterior door.

- $600 in total for exterior doors.

- Home energy audits are limited to $150.

Beginning in 2025, for each item of specified property placed in service, no credit will be allowed unless the item was produced by a QM and the taxpayer includes the PIN for the item on the taxpayer’s tax return.

Resources

- Publication 5967, Energy Efficient Home Improvement Credit (25C)

- Publication 5976, How to claim an Energy Efficient Home Improvement tax credit RESIDENTIAL ENERGY PROPERTY

- Publication 5978, How to claim an Energy Efficient Home Improvement tax credit HOME ENERGY AUDIT

- Publication 5979, How to claim an Energy Efficient Home Improvement tax credit EXTERIOR DOORS, WINDOWS, SKYLIGHTS AND INSULATION MATERIALS

![]() Issue 11: IR-2024-278 IRS Encourages all Taxpayers to Sign up for an IP PIN for the 2025 tax season

Issue 11: IR-2024-278 IRS Encourages all Taxpayers to Sign up for an IP PIN for the 2025 tax season

As the 2025 tax season approaches, the IRS encourages all taxpayers to take an important step to safeguard their identity by signing up for an Identity Protection Personal Identification Number (IP PIN).

This simple yet crucial step can provide an added layer of security, helping protect against tax-related identity theft.

The IRS encourages taxpayers to sign up for IRS Online Account, which provides a quick and easy way to obtain an IP PIN. Signing up early will ensure taxpayers have extra safety by having an IP PIN to electronically file their returns when the filing season begins in 2025.

The IRS encourages people to sign up for an IP PIN before Nov. 23, 2024. After this date, the IP PIN system will undergo maintenance and will not be available again until early January 2025. Signing up for an IP PIN now will ensure that a taxpayer’s identity is protected when the filing season begins. New IP PINs are generated for the 2025 filing season during this period, so online enrollees must retrieve their new IP PIN starting early January 2025.

An IP PIN is a six-digit number that prevents someone else from filing a federal tax return using a taxpayer’s Social Security number or Individual Taxpayer Identification Number. It’s a vital tool for ensuring the safety of taxpayers’ personal and financial information. The IP PIN, known only to an individual and the IRS, confirms their identity when they electronically file their tax return, making it much more difficult for thieves to use their information fraudulently.

How to request an IP PIN

The best way to sign up for an IP PIN is through IRS Online Account. The process requires identity verification, and spouses and dependents can also obtain an IP PIN if they complete the required verification steps. Once an IPPIN is issued, it must be on both electronic and paper returns.

To get an IP PIN, taxpayers should create or log into their online account at IRS.gov and follow the steps for identity verification. Once verified, taxpayers need to click on the profile tab to request their IP PIN. IP PIN users must use this number when filing their federal tax returns for the current calendar year and any previous years filed during that same period.

For those unable to create an Online Account, alternative methods are available, such as in-person authentication at a Taxpayer Assistance Center.

Additional information about IP PINs

- An IP PIN is valid for one calendar year. For security reasons, new IP PINs are generated at the beginning of each calendar year. Some participants will receive their IP PIN in the mail, while others will have to log into their Online Account to view their current IP PIN.

- Enrolled taxpayers can log back in to their Online Account to view their current IP PIN.

- Taxpayers with an IP PIN must use it when filing any federal tax returns during the year, including prior year tax returns, or amended returns.

- IP PIN users should share their number only with the IRS and their tax preparation provider. The IRS will never call, email, or text a request for the IP PIN.

- Taxpayers can get an IP PIN now for 2024. The IRS will issue new IP PINs starting in January 2025.

- Taxpayers who enrolled in the IP PIN program and have not been a victim of tax-related identity theft can opt out of the IP PIN program via their Online Account.

![]() Issue 12: IR-2024-276 IRS Announces Launch of Pass-through Compliance Unit in LB&I; New Group Brings Together Teams of Specialists from Across the Agency to Tackle Large or Complex Exams

Issue 12: IR-2024-276 IRS Announces Launch of Pass-through Compliance Unit in LB&I; New Group Brings Together Teams of Specialists from Across the Agency to Tackle Large or Complex Exams

The Internal Revenue Service announced that the new pass-through field operations unit has officially started work in its Large Business and International (LB&I) division to more efficiently conduct audits of pass-through entities.

The creation of a new unit specifically devoted to ensuring compliance of pass-throughs of every size and form — including partnerships, S-corporations and trusts — reflects the IRS’s broader efforts to focus more attention and resources on an area that has historically been under-scrutinized.

Previously, pass-through exams were divided between LB&I and the Small Business/Self-Employed (SB/SE) division based on the size of the entity.

Going forward, revenue agents in pass-through field operations will be assembled into geographically based teams that are responsible for primary exams of pass-through entity returns. LB&I will be responsible for starting pass-through exams, regardless of entity size. SB/SE will continue to examine pass-through entities as part of a related exam of a tax return.

Consolidating the case-working expertise and removing the entity-size barrier helps the IRS achieve its goal of increased audit rates in this complex area, streamlines workflows and provides more consistent experience for taxpayers.

A pass-through is a business entity in which the profits “pass through” to the owner(s) of that business and are taxed at the individual tax rate. They are frequently used by higher-income groups and can be complex tax arrangements.

Over the last year, LB&I has made strides building the foundation of this specialized group with internal and external hiring efforts to ensure its well-staffed with a blend of expertise from current IRS employees and new hires. In addition to staffing, the dedicated stand-up team also focused on collaboration between LB&I and SB/SE to review and enhance support frameworks, training programs and other internal processes.

The IRS has also embarked on other important changes to help dedicate resources and support to this complex compliance space.

- The IRS launched examinations of 76 of the largest partnerships with average assets over $10 billion that includes hedge funds, real estate investment partnerships, publicly traded partnerships, large law firms and many other industries. These audits can take years depending on the size and complexity of the partnerships.

- IRS Chief Counsel announced the creation of a new associate office that will focus exclusively on partnerships, S-corporations, trusts and estates. This office will be drawn from the current Pass-throughs and Special Industries (PSI) Office.

The stand-up of pass-through field operations meets one of the priorities of the Strategic Operating Plan under Objective Three: Fairness in Enforcement. It is also a significant part of the overall expanded enforcement efforts that focus on high-income and high-wealth individuals, partnerships and large corporations that have seen sharp drops in audit rates during the past decade.

![]() Issue 13: IRS Releases Notices on Expenses Treated as Amounts Paid for Medical Care and Preventive Care for Purposes of Qualifying as an HDHP Under § 223

Issue 13: IRS Releases Notices on Expenses Treated as Amounts Paid for Medical Care and Preventive Care for Purposes of Qualifying as an HDHP Under § 223

On October 17, 2024, the Internal Revenue Service (IRS) released Notice 2024-71 (Expenses Treated as Amounts Paid for Medical Care) and Notice 2024-75 (Preventive Care for Purposes of Qualifying as a High Deductible Health Plan (HDHP) under § 223).

Two notices released by the IRS added certain contraceptives to its lists of deductible medical expenses and preventative care benefits that can be provided by a high deductible health plan (HDHP) without a deductible.

Notice 2024-71 says the IRS will treat amounts paid for certain male contraceptives as amounts paid for medical care under §213. The section allows an itemized deduction for unreimbursed medical expenses paid during the tax year to the extent they exceed 7.5% of a taxpayer’s adjusted gross income. § 213 expenses may also be paid or reimbursed by health savings accounts, health reimbursement arrangements, health flexible spending arrangements and Archer medical savings accounts.

Notice 2024-75 adds over-the-counter oral contraceptives (including emergency contraceptives) and certain male contraceptives to the list of preventative care benefits that an HDHP can provide without charging a deductible. Additionally, the notice specifies:

- All types of breast cancer screening for individuals not diagnosed with breast cancer are treated as preventative care

- Continuous glucose monitors for individuals diagnosed with diabetes will generally be treated as preventative care

The safe harbor for insulin products provided without a deductible applies regardless of whether the product is prescribed to treat an individual diagnosed with diabetes or the insulin was prescribed for the purpose of preventing the exacerbation of diabetes or the development of a secondary condition

![]() Issue 14: Current PTINs Expire Dec. 31

Issue 14: Current PTINs Expire Dec. 31

All 2024 tax preparer tax identification numbers (PTINs) expire on Dec. 31. Anyone who prepares or assists in the preparation of federal tax returns for compensation must have a valid PTIN before preparing returns. Enrolled agents must also have a valid PTIN.

Preparers with a 2024 PTIN are being encouraged to use the online renewal process by logging into their online account. First-time applicants can also apply for a PTIN online. The non-refundable fee to renew or obtain a PTIN is $19.75 for 2025. Those who prefer a paper option can use Form W-12, IRS Paid Preparer Tax Identification Number (PTIN) Application and Renewal. However, it can take up to six weeks to process the paper form.

![]() Issue 15: What Are Mandatory 401(k) Roth Contributions Under the SECURE 2.0 Act?

Issue 15: What Are Mandatory 401(k) Roth Contributions Under the SECURE 2.0 Act?

We have heard that the SECURE 2.0 Act will require us to treat certain catch-up contributions under our 401(k) plan as Roth contributions. Can you tell us more about these mandatory Roth contributions?

As you know, if a 401(k) plan permits it, participants who are age 50 or older can make additional elective deferrals, known as “catch-up” contributions.

Under the SECURE 2.0 Act, catch-up contributions made beginning in 2026 by participants with FICA wages that exceeded $145,000 (as indexed) in the prior calendar year must be made to a designated Roth contribution account and cannot be made on a pretax basis. Amounts contributed to a designated Roth account are includible in gross income in the year of the contribution, but eligible distributions from the account (including earnings) are generally tax-free.

The SECURE 2.0 Act also provides that, if a plan allows eligible participants subject to this mandatory Roth tax treatment to make catch-up contributions, then all eligible participants must be permitted to make catch-up contributions as designated Roth contributions, even if they are not subject to the mandatory Roth tax treatment rule (e.g., a participant making $100,000). This means that a plan that currently does not offer participants a chance to elect designated Roth contributions soon may be required to, if catch-up-eligible participants will have compensation that exceeds the threshold.

This requirement was originally due to take effect in 2024; however, due to concerns that plans and service providers could not change their administrative and recordkeeping procedures in time to comply, the IRS provided for a two-year administrative transition period until 2026.

During this transition period, 401(k) plans may continue to allow all participants (including those with incomes above the threshold) to make pretax catch-up contributions and will be treated as satisfying the new requirements even if they do not provide for designated Roth contributions.

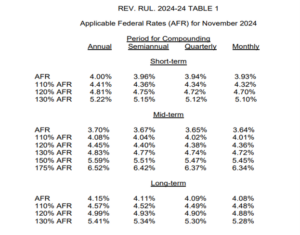

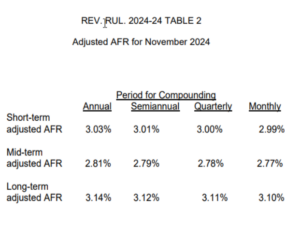

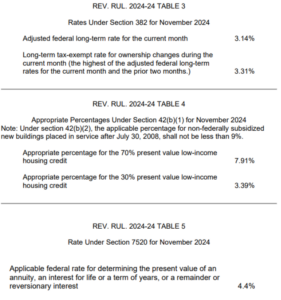

![]() Issue 16: Applicable Federal Rates for November 2024, Rev. Rul. 2024 – 24

Issue 16: Applicable Federal Rates for November 2024, Rev. Rul. 2024 – 24

![]() Basics & Beyond Resources

Basics & Beyond Resources

- Blog Page

- Resource List

- Webinar & Seminar Schedules

- Get Registered!

- Note: Paid attendees can request a link to the replay of any previously recorded webinar presentations by emailing us at [email protected]