Tax Newsletter: A New Year and a “NEW” 2021 Tax Filing Season

Are You Ready?

In This Issue

- Issue 1: 2021 Tax Filing Season Begins Feb. 12; IRS Outlines Steps to Speed Refunds During Pandemic

- Issue 2: Question and Answers from the 2021 January Quarterly Update

- Issue 3: Revenue Procedure 84-35 Changes

- Issue 4: CAA Extender and Temporary Relief Summary

- Issue 5: Notice 2021-11 – Deferral Period Changes

- Issue 6: Employer Provided Vehicle Temporary Relief Due to COVID-19

- Issue 7: Notice 2021-13 Partnerships Relief from Certain Penalties Due to Capital Account Balances

- Issue 8: Rev. Proc. 2021-1 User Fee Increases on Letter Rulings and Informational Letters

- Issue 9: More on Form Changes

- Issue 10: Submit Forms 2848 and 8821 Online FAQs

- Issue 11: Issue 11: Revenue Procedure 2021-11 Guidance on W-2 Filing Related to §199A(g)(1)(B)(i)

- Issue 12: All Taxpayers Now Eligible for Identity Protection PINs

- Issue 13: Waiver of Information Reporting Requirements with Respect to Certain Amounts Excluded from Gross Income

- Issue 14: FBAR Penalties Apply Per Form Rather Than Per Account Court Case – Will IRS Appeal?

- Issue 15: PPP Loan Forgiveness Application Form 3508-S is Available for Filing for Loans Under $150,000

- Issue 16: New President – New Tax Proposals – Update – What’s on the Table?

- Issue 17: Requesting Abatement under Reasonable Cause for Estimated Tax Penalty

- Issue 18: Chief Counsel Looks at 2016 Return Filed Late with the Long Extended 2020 Filing Season – Was a Refund Available?

- Issue 19: Form W-2 and Form 1099 Misc. Filed for the Same Year – IRS Guidance for the Examiner – Defining a Worker Classification Issue

- Issue 20: Applicable Federal Rates (AFR) for February 2021 – Rev. Rul. 2021-4

NEWS

Issue 1: 2021 Tax Filing Season Begins Feb. 12; IRS Outlines Steps to Speed Refunds During Pandemic

The Internal Revenue Service announced that the nation’s tax season will start on Friday, Feb. 12, 2021, when the tax agency will begin accepting and processing 2020 tax year returns.

The Feb. 12 start date for individual tax return filers allows the IRS time to do additional programming and testing of IRS systems following the Dec. 27 tax law changes that provided a second round of Economic Impact Payments and other benefits.

To speed refunds during the pandemic, the IRS urges taxpayers to file electronically with direct deposit as soon as they have the information they need.

Last year’s average tax refund was more than $2,500. More than 150 million tax returns are expected to be filed this year, with the vast majority before the Thursday, April 15 deadline.

Under the PATH Act, the IRS cannot issue a refund involving the Earned Income Tax Credit (EITC) or Additional Child Tax Credit (ACTC) before mid-February. The law provides this additional time to help the IRS stop fraudulent refunds and claims from being issued, including to identity thieves.

The IRS anticipates a first week of March refund for many EITC and ACTC taxpayers if they file electronically with direct deposit and there are no issues with their tax returns. This would be the same experience for taxpayers if the filing season opened in late January.

Overall, the IRS anticipates nine out of 10 taxpayers will receive their refund within 21 days of when they file electronically with direct deposit if there are no issues with their tax return. The IRS urges taxpayers and tax professionals to file electronically. To avoid delays in processing, people should avoid filing paper returns wherever possible.

Key Filing Season Dates

There are several important dates taxpayers should keep in mind for this year’s filing season:

- Jan. 15. IRS Free File opens. Taxpayers can begin filing returns through Free File partners; tax returns will be transmitted to the IRS starting Feb. 12. Tax software companies also are accepting tax filings in advance.

- Feb. 12. IRS begins 2021 tax season. Individual tax returns begin being accepted and processing begins.

- Feb. 22. Projected date for the IRS.gov Where’s My Refund tool being updated for those claiming EITC and ACTC, also referred to as PATH Act returns.

- First week of March. Tax refunds begin reaching those claiming EITC and ACTC (PATH Act returns) for those who file electronically with direct deposit and there are no issues with their tax returns.

- April 15. Deadline for filing 2020 tax returns.

- Oct. 15. Deadline to file for those requesting an extension on their 2020 tax returns.

Issue 2: Question and Answers from the 2021 January Quarterly Update

- Client did not apply for PPP1 because no payroll, can he apply for PPP2, still no payroll?

Answer: If self-employed can apply based on their net income but must apply for the PPP1. They are allowed to apply for the first loan.

- If a client had 2 employees in 2019 and early 2020 but ended 2020 with 4 employees (still having a 25% decrease in profit). For the PPP Loan 2, can they apply with the payroll with 4 employees?

Answer: Yes, make sure at least there is one quarter where there is a 25% decrease in gross Receipts.

- In 2020, OTC meds could be paid for with HSA, correct? So, when our program asks if all HSA distributions were used for medical expenses, can we say yes?

Answer: Under the original CARES Act (March 27, 2020), OTC medications may be reimbursed by HSA and FSA (Flexible Spending Accounts). This does not include vitamins.

- Are you saying that you have to have apply for loan forgiveness on the First PPP loan before you can apply for Round 2?

Answer: No, however, SBA will have to clear 1st loan if not yet forgiven before dispersing 2nd Round of PPP.

- The term clear??? In previous question. Does that mean they spent money on qualified expenses?

Answer: Yes

- Concerning the Employee Retention Credit. I have been reading that a lot of firms are not using 20% income decline but rather if client suffered impacts from COVID-19 due to vendor shutdowns, employee quarantines, etc. Do you have any guidance on that stance?

Answer: Employers, including tax-exempt organizations, are eligible for the credit if they operate a trade or business during calendar year 2020 and experience either:

- The full or partial suspension of the operation of their trade or business during any calendar quarter because of governmental orders limiting commerce, travel, or group meetings due to COVID-19, or

- A significant decline in gross receipts.

A significant decline in gross receipts begins:

- on the first day of the first calendar quarter of 2020.

- for which an employer’s gross receipts are less than 20% of its gross receipts.

- for the same calendar quarter in 2019.

The significant decline in gross receipts ends:

- on the first day of the first calendar quarter following the calendar quarter.

- in which gross receipts are more than of 80% of its gross receipts.

- for the same calendar quarter in 2019.

The credit applies to qualified wages (including certain health plan expenses) paid during this period or any calendar quarter in which operations were suspended.

- My son’s 2019 tax return has been delayed. Does it have to be accepted before he gets his Stimulus payment?

Answer: At this point he will need to file his 2020 return and get the stimulus payment at that time.

- I spent a lot of time trying to get into E-services to update my office address. When I tried to sign based on IRS instructions, I found my IRS-Tax Pro screen it did not look like the example. I have a username and password for PTIN but is it the same for e-services. I tried to call IRS and was on hold for almost two hours and got no answer. Can anyone help me with what to do? Amy answer can go directly to my e-mail of [email protected]. Thanks

Answer: You will need to call the e-services help line at: 866-255-0654.

- We got a letter from the lending bank saying that they will not even be ready to provide their papers for forgiveness till much later. The client got under $50,000.00 and will not qualify for the new loan due to the 25% income issue. What does a client due if the bank is not ready to process forgiveness on old loans when they really need the new one?

Answer: Loan payments are deferred only until 10 months after the last day of each borrower’s loan forgiveness covered period. {either 8- or 24-week period} If the business does not qualify for a Second PPP Loan due to the not meeting the 25% requirement, there is no other loan option. You cannot apply for a First Loan again.

- I am so sorry, I am so confused, I had PPP Loan under $50,000 and the bank is wanting documentation, but I just heard and am hearing that if under $50 or 150, then bank doesn’t need documentation.

Answer: The bank can ask for documentation as required by the SBA rules, but it cannot ask for documentation outside of those rules.

Example: You are self-employed with no employees, and you received a loan under PPP 1. Guidance stated that the bank can ask for bank statements, your Schedule C and a copy of the form 1099 MISC or 1099 NEC for example. The rules do not state that they can ask for how the money was spent because that PPP Loan was a “replacement of income.”

If you had employees, they could act for the Form 941, W-2 and request that you show it was paid for example. The new guidance mentioned in the power point details that. I would review.

- Do I wait for Round 1 forgiveness or do I apply and submit for forgiveness so we can apply for 3/31 Round 2 deadline?

Answer: Based on the guidance we have, which is not much, apply for the Second Round if you meet the criteria. SBA will not authorize disbursement of the Round 2 loan until Round 1 is forgiven. The Second loan will be held in suspense until that time. And then it will be processed.

- What if a business applied for Round 1, did not get approved, can they apply for Round 2?

Answer: This is how we answered this question. If they meet the 25% reduction rules, yes, they can apply, but remember the other rules needed to be meet for Round 2. We now believe that the answer was correct, but it would be nice to have additional guidance.

Note:

Looking at the application for the Second-Round where the client must initial and certify it states, “The Applicant received a First Draw Paycheck Protection Program Loan and, before the Second Draw Paycheck Protection Program Loan is disbursed, will have used the full loan amount (including any increase) of the First Draw Paycheck Protection Program Loan only for eligible expenses.” This implies that a First Round PPP Loan may be required. The applicant needs to certify in good faith to all of the items are true by initialing next to each one.

If no First Round was applied for, we suggest you reapply for Round 1. If only applying for Round Two we suggest instead of the initial to be placed beside that question requiring certification, we suggest that you use Not-Applicable (N/A).

As with the First Round, guidance is somewhat incomplete. It might be completed by the time/opportunity to applies ends. UGH! UGH!

- To clarify, an S corporation with one employee can apply for the PPP loan now even if they did not get the first one as long as they have the 25% reduction in a quarter. Do not need to have gotten PPP1.

Answer: Please review Question and Answer to #12.

- Is the first requirement to the Consolidated Appropriation Act that there had to be a 25% reduction in Gross Income for the year or for one quarter? I think that I understand that you have to compare the recognized quarters of 1st quarter to 1st quarter and you cannot compare 1st quarter to 4th Is that correct?

Answer: You have to compare the same quarter in 2019 with the same quarter in 2020. All four quarters could be down 25%, but you only need one quarter to qualify for a Round 2 PPP loan. Applicants must have been in operation on Feb. 15, 2020, to qualify. Self-employed business owners, including independent contractors, are also eligible for loans, but a rule imposed by the Small Business Administration requires sole proprietorships to have shown a profit on their 2019 tax return to qualify. They also have to show a certain amount of hardship: a 25% drop in gross receipts between comparable quarters in 2019 and 2020. They must also show that they used all of the money from the first loan in allowable ways.

Note: The $150K forgiveness app is supposed to be available on the 20th of January.

Issue 3: Revenue Procedure 84-35 Changes

IRS clarified sometime ago that Rev. Proc. 84-35 is still available to use for abatement of the failure to file penalty for partnerships if the criteria has been met. IRS has changed the way we need to address any abatement request. We have discussed this in one of our Quarterly Updates, but you may not have attended.

Reasonable cause for failure to file a timely and complete partnership return will be presumed if the partnership (or any of its partners) is able to show that all of the following conditions have been met. NOTE: the change is in bold.

The partnership had no more than 10 partners for the taxable year. (A husband and wife filing a joint return count as one partner.)

- Each partner during the tax year was a natural person (other than a non-resident alien), or the estate of a natural person.

- Each partner’s proportionate share of any partnership item is the same as his proportionate share of any other partnership item.

- The partnership did not elect to be subject to the rules for consolidated audit proceedings under IRC §§ 6221 through 6234.

- All partners reported their distributive share of partnership items on their timely filed income tax returns.

If all of the above conditions are met, you may return this notice with your statement, signed under penalty of perjury, that you qualify to have the penalty removed for reasonable cause under the provisions of Rev. Proc. 84-35.

The penalty can be reasserted if it was removed based on a statement with respect to Rev. Proc. 84-35, and it is later determined that such statement was false in any material respect. Additionally, a penalty for making false statements may be asserted under §7206.

- We must address the issue and state verbally (by phone) or in an abatement letter that the partnership did not elect to be subject to the rules for consolidated audit proceedings under IRC §§ 6221 through 6234.

It has been noted by other tax professional that the request for abatement will not be granted without this statement.

Issue 4: CAA Extender and Temporary Relief Summary

The Consolidated Appropriation Act (CAA) provided some extender provisions. The sections referred to below are sections of the CAA – not the IRC Code Sections. This list is not all inclusive.

- 101 – permanently reducing the medical expense reduction floor from 10% to 7.5%.

- 119 – extending §45S credit for paid family and medical leave.

- 120 – extending the addition of student loan payments to §127.

- §206 to 207 – extending and expanding the employee retention credit (ERC).

- 208 – allowing certain workers to receive in-service distributions from qualified plans.

- 209 – providing partial plan termination relief.

- 210 – temporarily allowing for full deduction for business meals provided by restaurants.

- 214 – temporarily relaxing flexible spending arrangement (FSA) rules.

- §301 to 303 – providing additional non-COVID-19 disaster relief.

In addition:

The Act’s changes other federal tax credit provisions, including:

Extending the following employment-related tax credits

The Work Opportunity Tax Credit (WOTC)

The Federal Empowerment Zone (FedEZ) credit for hiring and retention.

Issue 5: Notice 2021-11 – Deferral Period Changes

Notice 2021-11 provides that the end date of the period during which employers must withhold and pay the deferred taxes is postponed from April 30, 2021, to December 31, 2021, and associated interest, penalties, and additions to tax for late payment with respect to any unpaid deferred taxes will begin to accrue on January 1, 2022, rather than on May 1, 2021.

As required by §274 of the COVID-related Tax Relief Act of 2020, which was enacted as part of the Consolidated Appropriations Act, 2021, on December 27, 2020, this notice modifies Notice 2020 65 by extending the time period during which employers must withhold and pay certain taxes that were deferred under Notice 2020-65.

Issue 6: Employer Provided Vehicle Temporary Relief Due to COVID-19

In situations where due to COVID-19 pandemic and in spite of consistency rules otherwise required by §61 and the regulations, employers and employees using automobile lease valuation rule may instead use vehicle cents-per-mile valuation rule to determine value of employee’s personal use of employer-provided automobile beginning as of 3/13/2020.

This relief applies only if at beginning of 2020 calendar year, employer reasonably expected that automobile with FMV not exceeding $50,400 would be regularly used in employer’s trade or business throughout year, but due to pandemic automobile wasn’t regularly used in employer’s trade or business throughout 2020. In 2021, employers and employees may revert to lease valuation rule or continue to use vehicle cents-per-mile rule.

Due to the suddenness and unexpected onset of the COVID-19 pandemic, the Department of the Treasury and the Internal Revenue Service are providing relief from the consistency rules in §§1.61-21(d)(7) and 1.61-21(e)(5).

Therefore, employers that choose to switch from the automobile lease valuation rule to the vehicle cents-per-mile valuation rule in the 2020 calendar year must prorate the value of the vehicle using the automobile lease valuation rule for January 1, 2020, through March 12, 2020.

Employers should multiply the applicable Annual Lease Value by a fraction, the numerator of which is the number of days during the period beginning on January 1, 2020, and ending on March 12, 2020 (72 days), and the denominator of which is 365. As of March 13, 2020, employers may begin using the vehicle-cents-per-mile valuation rule. Employees using the automobile lease valuation rule whose employers switch from the automobile lease valuation rule to the vehicle cents-per-mile valuation rule under this notice must also switch to the vehicle cents-per-mile valuation rule.

Further, notwithstanding the consistency rules in §1.61-21(e)(5), employers that choose to switch from the automobile lease valuation rule to the vehicle cents-per-mile valuation rule during 2020 may revert to the automobile lease valuation rule for 2021, provided they meet the requirements of §1.61-21(d), other than the consistency rules in §1.61-21(d)(7).

Alternatively, employers that choose to switch to the vehicle cents-per-mile valuation rule during 2020 may continue using that rule for 2021, provided they meet the requirements of § 1.61-21(e), other than the consistency rules in §1.61-21(e)(5).

Employees that use one of the special valuation rules for vehicles must use the same special valuation rule for vehicles that is used by their employer.

The consistency rules in §1.61-21(e)(5) will apply as of January 1, 2021, as if January 1, 2021, were the first day the vehicle was used by the employee for personal use, and the consistency rules in §1.61-21(d)(7) will apply as of January 1, 2021, as if January 1, 2021, were the first day the vehicle was made available to the employee for personal use.

Accordingly, the special valuation rule used for 2021 must continue to be used by the employer and the employee for all subsequent years, except to the extent the employer uses the commuting valuation rule.

Employers that originally used the automobile lease valuation rule to calculate the value of the personal use of an employer-provided automobile during 2020 and that want to instead begin using the vehicle cents-per-mile valuation rule during 2020 based on the relief provided in this notice may use the rules in Announcement 85-113 for reporting and withholding on taxable noncash fringe benefits, or the adjustment process under §6413 or the refund claim process under §6402 to correct any overpayment of federal employment taxes on these benefits.

Issue 7: Notice 2021-13 Partnerships Relief from Certain Penalties Due to Capital Account Balances

Penalty relief from certain penalties due to the inclusion of incorrect information in reporting their partners’ beginning capital account balances on the 2020 Schedules K-1 (Form 1065) and the 2020 Schedules K-1 (Form 8865) as outlined in the 2020 Instructions for Form 1065, U.S. Return of Partnership Income.

Item L

The partnership must report the Beginning and Ending capital account for the year using the Tax Basis Method, including the amount of capital they contributed to the partnership during the year, their share of the partnership’s current year net income or loss as computed for tax purposes, any withdrawals and distributions made to them by the partnership, and any other increases or decreases to the capital account determined in a manner generally consistent with figuring the partner’s adjusted tax basis in its partnership interest (without regard to partnership liabilities), taking into account the rules and principles of §§705, 722, 733, and 742. The complete instruction when finalized can be found under Item L on page 7 of the 2020 Schedule K-1 Instructions.

This notice also provides relief from accuracy-related penalties for any taxable year for the portion of an imputed underpayment attributable to the inclusion of incorrect information in a partner’s beginning capital account balance reported by a partnership for the 2020 taxable year.

Issue 8: Rev. Proc. 2021-1 User Fee Increases on Letter Rulings and Informational Letters

The electronic submission procedures for ruling requests and non-automatic Forms 3115, Application for Change in Accounting Method, established temporarily in Rev Proc 2020-29, 2020-21 IRB 859, have been permanently incorporated in Rev Proc 2021-1, Sec. 16.

- 7.01(4) has been amended to clarify that a ruling request must state both whether the same issue is presented in any return and whether any such return is currently or was previously under examination.

- §7.04(1), 8.01, 9.05(1), and 9.07 have been updated to reflect that ruling and change of accounting method requests should now be addressed to and will be initially controlled by the Technical Services Support Branch of the Legal Processing Division within Associate Chief Counsel (Procedure & Administration).

- 9.06 has been updated to permanently allow taxpayers filing automatic Forms 3115 under the provisions of Rev Proc 2015-13, to submit the duplicate copy of the Form 3115 by fax.

Appendix A, Schedule of User Fees, has been amended with revised user fees reflecting costs incurred by the IRS to administer the ruling program.

Issue 9: More on Form Changes

1040 and 1040-SR Instructions for Tax Year 2020

The IRS has released a new draft of the instructions for Form 1040 and Form 1040-SR, U.S. Tax Return for Seniors, that incorporates recently legislative changes made by the Consolidated Appropriations Act, 2021 (CAA, 2021, PL 116-260). The draft instructions also contain other new information including information about virtual currency reporting.

Virtual Currency Guidance

The IRS further defined what a Virtual Currency Transaction is and is not. A transaction involving virtual currency does not include the holding of virtual currency in “a wallet or account,” or the transfer of virtual currency from one wallet or account the taxpayer owns or controls to another that the taxpayer owns or controls.

The instructions also noted that, “A transaction involving virtual currency includes but is not limited to:

- The receipt or transfer of virtual currency for free (without providing any consideration), including from an airdrop or following a hard fork.

- An exchange of virtual currency for goods or services.

- A sale of virtual currency; and

- An exchange of virtual currency for other property, including for another virtual currency.”

- An acquisition or disposition of a financial interest in • An acquisition or disposition of a financial interest in virtual currency.”

Economic Stimulus Payments

The instructions now refer to the first round of EIPs provided by the CARES Act as EIP 1 and the second round provided by COVIDTRA as EIP 2. In addition, “Any economic impact payments received are not taxable for federal income tax purposes, but they reduce the recovery rebate credit.”

The Term “Recovery Rebate Credit”

The credit is figured like EIP 1 and EIP 2, except eligibility and the amount of the credit are based on the taxpayer’s tax year 2020 information. The instructions include a Recovery Rebate Credit Worksheet to figure a taxpayer’s credit amount.

Other Changes

CAA, 2021 also provided certain other tax-related benefits that are discussed in the instructions.

- Election to use 2019 earned income to figure 2020 earned income credit.

- Election to use 2019 earned income to figure 2020 additional child tax credit.

- Educator expenses include amounts paid or incurred after March 12, 2020, for personal protective equipment, disinfectant, and other supplies used for the prevention of the spread of coronavirus.

- If a taxpayer was impacted by certain federally declared disasters, special rules may apply to distributions from the taxpayer’s IRA, profit-sharing plan, or retirement plan.

Form 4952 Changes.

The instructions for Form 4952 state that if a taxpayer is filing Form 4952, Investment Interest Expense Deduction, and the taxpayer has an amount on line 4e (the smaller of the taxpayer’s:

- net gain from the disposition of property held for investment or

- net capital gain from the disposition of property held for investment) or

- 4g (certain amounts elected to be included in investment income).

Then the taxpayer must use the Schedule D Tax Worksheet in the Instructions for Schedule D, Capital Gains and Losses, to figure the taxpayer’s tax, even if the taxpayer does not need to file Schedule D.

Issue 10: Submit Forms 2848 and 8821 Online FAQs

What is an electronic signature?

An electronic signature is a way to get approval on electronic documents. It can be in many forms and created by many technologies. You do not need specific technology to create electronic signatures.

Electronic signatures can be:

- A typed name that is typed on a signature block.

- A scanned or digital image of a handwritten signature attached to an electronic record.

- A handwritten signature inputted onto an electronic signature pad.

- A handwritten signature, mark or command inputted on a display screen with a stylus device.

Is an electronic signature the same as a digital signature?

No. An electronic signature is an electronic symbol attached to an electronic record that a person will sign. A digital signature is a type of an electronic signature.

Who needs to be authenticated?

You must authenticate a taxpayer’s identity when the taxpayer electronically signed the form in a remote transaction (e.g., not in your presence) and you do not have a personal or business relationship with the taxpayer.

How do I authenticate a taxpayer’s identity?

If you do not know a taxpayer personally or you haven’t done business with them, you must verify their identity if they’re signing the form to do a remote transaction.

To authenticate the taxpayer’s identity for remote transactions, take these steps:

- Inspect a valid government photo identification (ID) of the taxpayer and compare the photo to the taxpayer.

- Use a self-taken picture of the taxpayer or video conferencing to compare.

Examples of government photo ID:

A driver’s license, employer ID, school ID, state ID, military ID, national ID, voter ID, visa or passport.

Record the name, Social Security number or Individual Taxpayer Identification Number, address and date of birth of the taxpayer.

Verify the taxpayer’s name, address and Social Security number or Individual Taxpayer Identification Number (TIN) using secondary documentation, such as a federal or state tax return, IRS notice or letter, Social Security card or credit card or utility statement.

- For example, if a taxpayer changed their address in 2020, a 2019 tax return can be used to verify the taxpayer’s name and TIN, and a recent utility statement to verify the taxpayer’s address.

Should I keep proof that I authenticated the taxpayer’s identity ?

- After you record the name, Social Security Number or Individual Taxpayer Identification Number, address, and date of birth of the taxpayer, retain this record, so it is available upon IRS request.

- You are required to retain this record for seven years.

Can I use my Secure Access account for e-Services/TDS/SOR to log in to the TDC platform?

Yes. If you already registered for a Secure Access account for IRS tools such as e-Services, Get Transcript or Get an IP PIN, you may use the same account to log in to the TDC platform. I

if you don’t have an account, register now for Secure Access if you want to use the TDC platform beginning in January 2021.

I can’t create a Secure Access account. What should I do?

To create an account, you must successfully authenticate your identity using Secure Access.

For more information, see IRS.gov/SecureAccess.

If you are unable to validate your identity, you may get ink signatures on the authorization forms and send them to the appropriate location based on the “Where to File Chart” using mail or fax. (Form 2848 Where to File Chart & Form 8821 Where to File Chart)

Can I fax an electronically signed form to the IRS?

No. All forms mailed or faxed to the IRS must have “wet” ink signatures.

I previously submitted my electronically-signed form on TDC, can I call IRS to discuss my client’s case?

Yes, if the form has been processed and after the IRS employee performs the standard telephone authentication. If the form has not been processed, for security reasons, you must follow normal procedures to fax a copy of the form with a “wet” ink signature before the case can be discussed.

If you fax a copy of the form with a “wet” ink signature to the Practitioner Priority Service (PPS), you will be able to speak with a representative immediately. If you fax a copy of the form with a “wet” ink signature to the Centralized Authorization File (CAF) Unit, you will have to wait for the form to be processed before being able to speak with a representative.

Why must I enter the taxpayer’s TIN before I can upload the form?

IRS uses the taxpayer’s TIN to match the digital upload and form.

What do I need to know to upload the forms?

Follow this guidance when you upload Forms 2848 or 8821: Save the forms following:

- 15MB file size limit .pdf, .jpeg, .jpg, .gif file formats.

- Upload one form at a time. Do not create one combined file

I can’t attach my forms within the TDC platform. Who do I call?

IRS does not offer telephone support for the TDC platform.

For help, review common errors or have the taxpayer sign the authorization form with an ink signature and fax the form to the IRS.

Will I receive confirmation when my form is received?

Yes. The IRS will send you an email confirmation when the form is successfully submitted.

Will I receive notification when my form is processed?

No. You will not be notified when the form is processed. However, the IRS will send you and the taxpayer a letter via the U.S. Postal Service if the form is rejected.

Will my forms get processed faster using this system?

- IRS processes forms in the order they receive them regardless of the submission method (e.g., mail, fax, online) they are received.

- Forms submitted online are reviewed and processed by IRS employees in the same manner as those received via fax or mail.

Why do I have to submit my forms one at a time?

Due to the way IRS processes forms, you can only upload one at a time. You may upload more forms at the end of each session.

I have more than two designees on the Form 8821, what do I do?

- If you want to name more than two designees, check the box on line 2 and attach a list of designees to the Form 8821.

- Provide the address and requested numbers for each designee named.

- Attach the list of designees to the Form 8821.

- Upload the Form 8821 (with the list of designees) once finished.

Can the TDC platform be used to revoke or withdraw an authorization form?

Yes. See the revocation or withdrawal procedures in the form instructions or in Publication 947, Practice Before the IRS and Power of Attorney.

- To revoke authorization as a taxpayer, write the word “revoke” across the original Form 2848 or 8821.

- Under the word “revoke,” sign and write the date.

- To withdraw authorization as a representative, write the word “withdraw” across the Form 2848 or 8821.

- Under the word “withdraw,” sign and write the date.

Why is the IRS launching the TDC platform now?

IRS created this capability on the TDC platform to reduce in-person contact during the Coronavirus (COVID-19) pandemic.

How will the Tax Pro Account be different from this process?

The Tax Pro Account will be an all-digital platform. Tax professionals can initiate a request for authorization from their account and it will send to the client’s online account for an electronic signature. The client will access their account, electronically sign the authorization and the system will send it to the CAF database.

Issue 11: Revenue Procedure 2021-11 Guidance on W-2 Filing Related to §199A(g)(1)(B)(i)

Rev. Proc. 2021-11, provides methods for calculating W-2 wages for purposes of §199A(g)(1)(B)(i), which, for certain specified agricultural or horticultural cooperatives provides a limitation based on W-2 wages to the amount of a deduction under §199A(g)(1)(A) of 9% of the lesser of qualified production activities income or taxable income of a Specified Cooperative. This Revenue Procedure also modifies Revenue Procedure 2019-11, to amend the method for determining W-2 wages for taxpayers with short taxable years.

For taxpayers above a certain amount of taxable income, §199A(b)(2) limits the amount of a taxpayer’s §199A deduction for each qualified trade or business to the lesser of:

- 20% of the taxpayer’s QBI with respect to the qualified trade or business, or

- the greater of:

- 50% of the W-2 wages with respect to the qualified trade or business, or

- the sum of 25% of the W-2 wages with respect to the qualified trade or business plus 2.5% of the unadjusted basis immediately after acquisition of all qualified property.

The Code defines term “W-2 wages” to mean, with respect to any person for any tax year of such person, the amounts paid by such person with respect to employment of employees by such person during the calendar year ending during such tax year. W-2 wages does not include any amount which is not properly allocable to qualified business income and provides that W-2 wages do not include any amount that is not properly included in a return filed with the Social Security Administration (SSA) on or before the 60th day after the due date (including extensions) for such return.

- 199A(g) provides a deduction for a specified agricultural and horticultural cooperative equal to 9% of the lesser of:

- qualified production activities income (QPAI) for the tax year; or

- the specified cooperative’s taxable income for the tax year.

The deduction is limited to 50% of the specified cooperative’s W-2 wages for the tax year.

W-2 wages are determined in the same manner as under §199A(b)(4), except that such wages do not include any amount that is not properly allocable to domestic production gross receipts (DPGR). DPGR are, generally, the gross receipts of a taxpayer which are derived from any lease, rental, license, sale, exchange, or other disposition of any agricultural or horticultural product which was manufactured, produced, grown, or extracted by the taxpayer in whole or significant part within the United States.

The IRS issued a revenue procedure for calculating W-2 wages for purposes of §199A(b)(4)(A). The guidance provides three methods for calculating W-2 wages: the unmodified Box method, the modified Box 1 method, and the tracking wages method.

Issue 12: All Taxpayers Now Eligible for Identity Protection PINs

The Internal Revenue Service has expanded the Identity Protection PIN Opt-In Program to all taxpayers who can verify their identities.

The Identity Protection PIN (IP PIN) is a six-digit code known only to the taxpayer and to the IRS. It helps prevent identity thieves from filing fraudulent tax returns using a taxpayers’ personally identifiable information.

The IRS launched the IP PIN program nearly a decade ago to protect confirmed identity theft victims from ongoing tax-related fraud. In recent years, the IRS expanded the program to specific states where taxpayers could voluntarily opt into the IP PIN program. Now, the voluntary program is going nationwide.

About the Ip Pin Opt-In Program

Here are a few key things to know about the IP PIN Opt-In program:

- This is a voluntary program.

- You must pass a rigorous identity verification process.

- Spouses and dependents are eligible for an IP PIN if they can verify their identities.

- An IP PIN is valid for a calendar year.

- You must obtain a new IP PIN each filing season.

- The online IP PIN tool is offline between November and mid-January each year.

- Correct IP PINs must be entered on electronic and paper tax returns to avoid rejections and delays.

- Your client should never share the IP PIN with anyone but their trusted tax provider. The IRS will never call, text or email requesting the IP PIN. Beware of scams to steal the IP PIN.

- There currently is no opt-out option but the IRS is working on one for 2022.

How to get an IP Pin

Taxpayers who want an IP PIN for 2021 should go to IRS.gov/IPPIN and use the Get an IP PIN tool. This online process will require taxpayers to verify their identities using the Secure Access authentication process if they do not already have an IRS account. There is no need to file a Form 14039, an Identity Theft Affidavit, to opt into the program.

Once taxpayers have authenticated their identities, their 2021 IP PIN immediately will be revealed to them. Once in the program, this PIN must be used when prompted by electronic tax returns or entered by hand near the signature line on paper tax returns.

All taxpayers are encouraged to first use the online IP PIN tool to obtain their IP PIN. Taxpayers who cannot verify their identities online do have options.

Taxpayers whose adjusted gross income is $72,000 or less may complete Form 15227, Application for an Identity Protection Personal Identification Number, and mail or fax to the IRS. An IRS customer service representative will contact the taxpayer and verify their identities by phone. Taxpayers should have their prior year tax return at hand for the verification process.

Taxpayers who verify their identities through this process will have an IP PIN mailed to them the following tax year. This is for security reasons. Once in the program, the IP PIN will be mailed to these taxpayers each year.

Taxpayers who cannot verify their identities online or by phone and who are ineligible for file Form 15227 can contact the IRS and make an appointment at a Taxpayer Assistance Center to verify their identities in person. Taxpayers should bring two forms of identification, including one government-issued picture identification.

Taxpayers who verify their identities through the in-person process will have an IP PIN mailed to them within three weeks. Once in the program, the IP PIN will be mailed to these taxpayers each year.

No change for confirmed identity theft victims

Taxpayers who are confirmed identity theft victims or who have filed an identity theft affidavit because of suspected stolen identity refund fraud will automatically receive an IP PIN via mail once their cases are resolved. Current tax-related identity theft victims who have been receiving IP PINs via mail will experience no change.

Issue 13: Waiver of Information Reporting Requirements with Respect to Certain Amounts Excluded from Gross Income

Notice 2021-06, waives the requirement to file certain information returns or furnish certain payee statements otherwise required by the Internal Revenue Code (Code) pursuant to §279 of the COVID-related Tax Relief Act of 2020 (COVID Relief Act).

Specifically, this notice waives the requirement to file certain information returns or furnish certain payee statements otherwise required by §61 of the Code with respect to amounts excluded from gross income by reason of §7A(i) of the Small Business Act, PPP Loans.

The notice does not waive information reporting requirements to file and furnish Forms 1098 and 1098-T with respect to those amounts.

Issue 14: FBAR Penalties Apply Per Form Rather Than Per Account Court Case – Will IRS Appeal?

A district court has found that the $10,000 non-willful FBAR penalty (for failure to file the FBAR) applies per FBAR form, not per bank accounts the individual or entity have which are required to be reported on the form. (Bittner v. United States, No. 4:19-cv-0415 (E.D. Tex. 6/29/20))

What is FBAR?

Every U.S. person that has a financial interest in, or signature or other authority over, a financial account, or accounts, in a foreign country must report the account, or accounts, to IRS annually on a FinCEN Report 114, Report of Foreign Bank and Financial Accounts (commonly referred to as an FBAR or FBAR form) if the aggregate value of the foreign financial accounts exceeds $10,000 at any time during the calendar year.

One FBAR is used to report multiple foreign financial accounts.

The penalty for violating the FBAR requirement is set forth in 31 USC § 5321(a)(5). The amount of the penalty depends on whether the violation was non-willful or willful.

The maximum penalty amount for a non-willful violation of the FBAR requirements started at $10,000 and has been adjusted for inflation yearly.

| U.S. Code citation | Civil Monetary Penalty Description | Current Maximum |

| 31 U.S.C. 5321(a)(5)(B)(i) | Foreign Financial Agency Transaction – Non-Willful Violation of Transaction | $12,921 per account / year |

| 31 U.S.C. 5321(a)(5)(C) | Foreign Financial Agency Transaction – Willful Violation of Transaction | Greater of $129,210, or 50% of the amount per 31 U.S.C.5321(a)(5)(D) |

The U.S. District Court for the Eastern District of Texas was not convinced that Bittner had reasonable cause for failing to report his accounts more than 16 years after he should have first filed an FBAR.

The court also did not agree with the government’s argument that he should be subject to the $10,000 penalty for every account that he failed to report for a total of $1.77 million.

The Bittner decision is a win for the taxpayer. However, it remains to be seen whether the government will appeal the decision. Another court agrees with the Bittner ruling, yet a different court takes the IRS stance. Therefore, this issue is unsettled. We await the IRS determination on whether they will appeal.

Bottom Line: Get Your Clients in Compliance

Issue 15: PPP Loan Forgiveness Application Form 3508-S is Available for Filing for Loans Under $150,000

The Borrower can apply for forgiveness of the First or Second Draw Paycheck Protection Program (PPP) Loan using this SBA Form 3508EZ if the PPP loan amount loan amount is $150,000 or less. Do not submit this Checklist with the SBA Form 3508-S. Each PPP loan must use a separate loan forgiveness application form. You cannot use one form to apply for forgiveness of both a First Draw PPP Loan and a Second Draw PPP loan.

If the client is eligible to use this form, they must apply for forgiveness of the PPP loan using SBA Form 3508 or 3508EZ (or lender’s equivalent form).

Each PPP loan must use a separate loan forgiveness application form. You cannot use one form to apply for forgiveness of both a First and Second Draw PPP loan.

Issue 16: New President – New Tax Proposals – Update – What is on the Table?

Domestic Taxes

- Raise the top corporate income tax rate to 28% from 21%.

- Taxing capital gains and dividends as ordinary income for those with annual incomes of more than $1 million.

- Setting a 15% minimum tax on the book income of corporations with book income greater than $100 million.

International Tax

Supports measures of that would discourage off-shoring and encourage on-shoring.

Increasing the tax rate on profits earned by foreign subsidiaries of US firms by increasing the global intangible low-taxed income (GILTI) tax rate to 21% and applying the regime on a per-country basis.

Creating a “Made in America” tax credit to offset 10% of investments geared toward creating jobs in the US and introducing a surtax on certain goods and services imported into the US.

Extender Possibilities

A bill could also include a significant “extenders” package addressing expiring tax provisions, making several provisions permanent and aligning others with the scheduled expiration of tax cuts under the Tax Cuts and Jobs Act.

Issue 17: Requesting Abatement under Reasonable Cause for Estimated Tax Penalty

26 U.S. Code § 6654 – Failure by individual to pay estimated income tax.

With 2020 behind us, many of our client could receive estimated tax penalties due to the “uncertainty” placed on many businesses as well as investment funds due to COVID-19. Some businesses have thrived while others are barely staying afloat even with the help of the PPP Loan Program.

- 6654(e) (3)(A) allows for a waiver in certain cases. It states, “ No addition to tax shall be imposed under subsection (a) with respect to any underpayment to the extent the Secretary determines that by reason of casualty, disaster, or other unusual circumstances the imposition of such addition to tax would be against equity and good conscience.”

IRS has stated there would be no blanket waivers and we must apply under reasonable cause based on the facts and circumstances of the client.

- First evaluate the client circumstances, after all the President did Declare a National Emergency Concerning the Novel Coronavirus Disease (COVID-19) Outbreak. This declaration of a national emergency could be interpreted as a National Disaster.

- Once the penalty notice is received make sure that:

- Use the attached envelope with the notice to respond for forgiveness. It has a barcode that will send the letter to appropriate IRS group that handles the abatement process.

- Make sure your letter states the reason why the client has been unable to either meet the due dates of the estimates but was able to at least pay 100% of last year’s tax or

- If income was down, state the percentage.

An example of a potential letter is below:

Date

IRS Office

Taxpayer’s Name, Address

TIN

Tax year

Note the Notice or Letter Number

The above taxpayer underpaid Federal estimated tax payments this year (2020) due to reasonable cause. Internal Revenue Code § 6654(e)(3)(A) allows waiver of the underpayment penalty due to disaster. On March 13, 2020, the President of the United States issued a Proclamation “Declaring a National Emergency Concerning the Novel Coronavirus Disease (COVID-19) Outbreak.”

Due to the circumstances surrounding the COVID-19 virus the taxpayer was unable to perform normal daily tasks such as banking, employment and day to day living activities. This includes operating a business with the current uncertainty and periodic shutdowns and was unable to timely pay Federal estimated income tax payments for 2020.

We hereby request a waiver under equitable circumstances of the underpayment penalty.

Issue 18: Chief Counsel Looks at 2016 Return Filed Late with the Long Extended 2020 Filing Season – Was a Refund Available? CCA 202053015

In this case the taxpayer was entitled to a refund due to the extended due date for 2019 Tax Year of July 15, 2020. An example has been provided.

Henry and Wilma

Taxpayer had withholding from 2016 deemed paid on 4/15/2017.

Taxpayer late filed 2016 return in June of 2020 and claimed a refund of the withholding that was deemed paid on 4/15/17.

The taxpayer’s 2016 refund claim (in this case on a delinquent return) was due by 4/15/20 in order to claim the withholding deemed paid on 4/15/17.

Yet Notice 2020-23 postponed the due date to 7/15/20. So, when the taxpayer filed in June of 2020, the refund claim was timely. And the postponement operated to disregard the period of 4/15/20 to the date of filing in June of 2020 for purposes of the §6511 look-back period. Review these examples from Treas. Reg. 301.7508A-1, as it illustrates the same principle:

Example 1

Henry and Wilma, residents of Polk County in the United States, intend to file an amended return to request a refund of 2008 taxes.

Henry and Wilma timely filed their 2008 income tax return on April 15, 2009. Under §6511(a), the amended 2008 return must be filed on or before April 16, 2012 (because April 15, 2012 falls on a Sunday, the amended return was due to be filed on April 16, 2012).

On April 2, 2012, an earthquake strikes Polk County. On April 6, 2012, certain counties in the U.S. (including Polk County are determined to be disaster areas within the meaning of §1033(h)(3) that are eligible for assistance by the Federal government under the Stafford Act.

In addition, on April 6, 2012, the IRS determines that Polk County is a covered disaster area and publishes guidance announcing that the time period for affected taxpayers to file returns, pay taxes, and perform other time-sensitive acts falling on or after April 2, 2012, and on or before October 2, 2012, has been postponed to October 2, 2012.

Filing a claim for refund of tax is one of the taxpayer acts for which the IRS may disregard a period of up to one year. The postponement period for this disaster begins on April 2, 2012 and ends on October 2, 2012.

Accordingly, Henry and Wilma’s claim for refund for 2008 taxes will be timely if filed on or before October 2, 2012.

In applying the lookback period in §6511(b)(2)(A), which limits the amount of the allowable refund, the period from October 2, 2012, back to April 2, 2012, is disregarded.

Thus, if the claim is filed on or before October 2, 2012, amounts deemed paid on April 15, 2009, under §6513(b), such as estimated tax and tax withheld from wages, will have been paid within the lookback period of §6511(b)(2)(A)

Also remember in 2020 we had specific guidance on when estimated tax should have been deposited.

Issue 19: Form W-2 and Form 1099 Misc. Filed for the Same Year – IRS Guidance for the Examiner – Defining a Worker Classification Issue

When the taxpayer files both Form W-2 and Form 1099-MISC. for a worker, the examiner should consider whether:

- The worker was treated as an employee for part of the year and an independent contractor for a separate part of the year (i.e., payments reported on Form W-2 and Form 1099-MISC were for the same services but distinct periods of time during the year).

- The worker was performing two or more distinct services and the taxpayer considered the worker to be an employee for one service and an independent contractor for the other service (i.e., dual status worker).

- The payment reported on Form 1099-MISC represented additional compensation to the worker in his capacity as an employee for which he received compensation reported on Form W-2 (e.g., a bonus payment).

Worker was treated as an employee for part of the year.

Examiners often encounter situations where a worker was treated as an employee for part of the year and an independent contractor for a separate part of the year.

The examination of whether the worker should have been treated as an employee for the period of time the worker was treated as an independent contractor is a worker classification issue.

The fact that the taxpayer treated the worker as an employee for part of the year does not turn the examination of the period of time the worker was treated as an independent contractor into a wage issue.

Example 1

The taxpayer treated the workers as employees from January 1, 2019, through June 30, 2019. All compensation paid to workers for this period was reported as wages on Forms 941 and the taxpayer filed Forms W-2 reporting the compensation paid to the workers for this period.

The taxpayer reclassified the workers as independent contractors beginning on July 1, 2019 and continued to treat the workers as independent contractors for the remainder of 2019. The compensation paid to the workers for the period from July 1, 2019, through December 31, 2019, was reported on Forms 1099-MISC as non-employee compensation in box 7.

The workers performed the same services and there was no change in control factors for the period from July 1, 2019, through December 31, 2019.

Since the taxpayer treated the workers as independent contractors for a period of time distinct from the period of time the workers were treated as employees, an examination of the status of the workers for July 1, 2019, through December 31, 2019 is a worker classification issue.

Dual Status Workers – A Worker Classification Issue

When a taxpayer files both a Form W-2 and Form 1099-MISC for a worker for the same year, and payments reported on each information return were made during the same period of time, the taxpayer may argue that the worker was performing two separate and distinct services – one as an employee and one as an independent contractor.

Examiners must develop the facts to determine whether the workers were truly performing separate and distinct services as an employee and independent contractor. The examination of whether the worker was clearly performing separate and distinct services, and whether the worker was an employee for Form 1099-MISC services, is a worker classification issue.

The facts relating to Form W-2 services would not be considered in deciding whether the worker is an employee for Form 1099-MISC services. If the worker was not performing separate and distinct services concurrently, the issue will be a wage issue, not a worker classification issue.

Example 2

During an employment tax examination, the examiner found the taxpayer filed both a Form W-2 and Form 1099-MISC in the same year for a worker.

The taxpayer explained that the worker performed dual services. The worker was treated as an employee for services performed as an auto mechanic. The worker was treated as an independent contractor for services performed as a car salesman.

The examiner determined that the worker performed services as an auto mechanic on Monday through Thursday each week and as a car salesman on Friday and Saturday.

As an auto mechanic, the worker was paid an hourly rate of $40 per hour which was reported on Form W-2. As a car salesman, the worker was paid only a commission for each car sold. The examiner verified the commission payments based on sales records and confirmed these amounts were reported on Form 1099-MISC.

The examination of whether the worker should have been treated as an employee for services performed as a car salesman is a worker classification issue. The fact that the worker was treated as an employee for services performed as an auto mechanic is not relevant to the issue of whether the worker is an employee for services performed as a car salesman. Only the facts specific to his services as a car salesman must be analyzed to determine whether the worker is an employee with respect to services as a car salesman.

Example 3

During an examination of a taxpayer’s 2019 employment tax returns, the examiner found the taxpayer filed both Form W-2 and Form 1099-MISC for several workers.

The taxpayer explained that the workers were mortgage brokers performing dual services. The taxpayer considered the workers to be independent contractors for selling mortgages, and employees for the time spent completing the paperwork to process the mortgages.

The workers were paid a flat hourly rate for all services; however, the taxpayer allocated the compensation to the workers as 80% for selling mortgages and 20% for completing paperwork.

The examiner concluded that completing the paperwork to process the mortgages sold is part of the same services provided by the workers for selling the mortgages. Since only one service is provided, these are not dual status workers. The examination is a wage issue because the compensation reported on Form 1099-MISC was for the same services for which wages were reported on Form W-2.

Additional Compensation Payments Reported on Forms 1099-MISC

When a taxpayer files both Form W-2 and Form 1099-MISC for a worker for the same year, and the payment reported on Form 1099-MISC can clearly be identified as additional compensation (such as a taxable fringe benefit), the examination of whether the additional compensation is subject to employment tax is a wage issue. The consideration is whether the payment meets the definition of wages or is excludable under a specific Code section.

Example 4

During an examination of the taxpayer’s 2019 employment tax returns, the examiner found the taxpayer filed both Form W-2 and Form 1099-MISC for several workers. The taxpayer explained that the amounts reported on the Forms 1099-MISC were year-end bonuses paid to employees. Since bonuses were paid to workers for services performed as employees, the bonus payments are considered additional wages subject to employment taxes. The examination would not be considered a worker classification issue.

Issue Indicators or Audit Tips

- Prior to contacting the taxpayer, the examiner should review the tax returns and IDRS information to identify potential issues. This may include reviewing Forms W-2 and 1099 filings to identify potential worker classification issues, or whether the taxpayer is filing both Forms 1099-MISC and Forms W-2 for any worker.

- Compare Forms W-2 to Forms 1099 to see if the taxpayer filed both forms for any worker.

- Inquire during taxpayer interviews whether they have workers paid both as an employee and contractor.

- Review the organizations payables for payments to the same workers for different categories, such as salary and then also as “contract”.

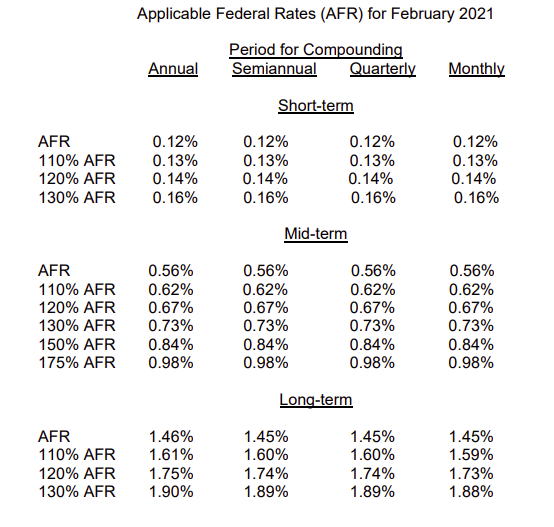

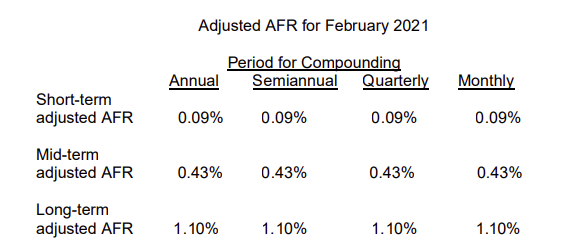

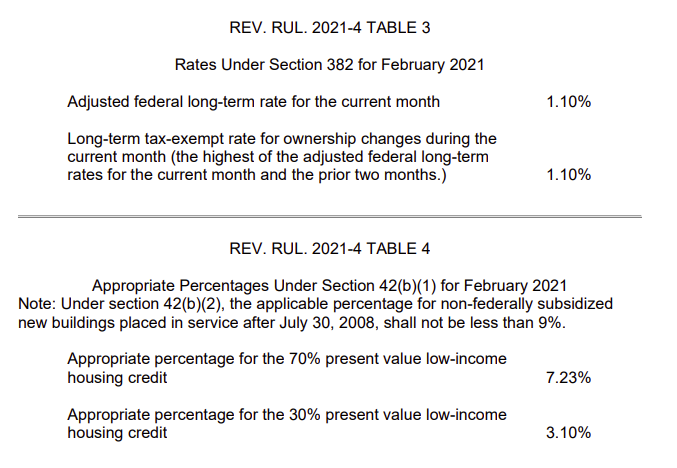

Issue 20: Applicable Federal Rates (AFR) for February 2021 – Rev. Rul. 2021-4

Rev. Rul. 2021-4 Table 2

![]() Basics & Beyond Resources

Basics & Beyond Resources

- Blog Page

- Resource List

- Webinar & Seminar Schedules

- Get Registered!

- Note: Paid attendees can request a link to the replay of any previously recorded webinar presentations by emailing us at [email protected]