Issue 1: Individuals with Significant Tax Debt Should Act Promptly to Avoid Revocation of Passports

Clients should resolve their significant tax debts to avoid putting their passports in jeopardy. They should contact the IRS now to avoid delays in their travel plans later.

Under the Fixing America’s Surface Transportation (FAST) Act, the IRS notifies the State Department of clients certified as owing a seriously delinquent tax debt, which is currently $52,000 or more. The law then requires State Department to deny their passport application or renewal. If a client currently has a valid passport, the State Department may revoke the passport or limit a client’s ability to travel outside the United States.

When the IRS certifies a client to the State Department as owing a seriously delinquent tax debt, the taxpayer receives a Notice CP508C from the IRS. The notice explains what steps the client needs to take to resolve the debt. IRS telephone assistors can help taxpayers resolve the debt. For example, they can help client set up a payment plan or make them aware of other payment options.

It’s especially important for client’s with imminent travel plans who have had their passport applications denied by the State Department to call the IRS promptly. The IRS can help your client resolve their tax issues and expedite reversal of their certification to the State Department. When expedited, the IRS can generally shorten the 30 days processing time by 14 to 21 days. For expedited reversal of their certification, clients will need to inform the IRS that they have travel scheduled within 45 days or that they live abroad.

For expedited treatment, taxpayers must provide the following documents to the IRS:

Proof of travel. This can be a flight itinerary, hotel reservation, cruise ticket, international car insurance or other document showing location and approximate date of travel or time-sensitive need for a passport.

Copy of letter from the State Department denying their passport application or revoking their passport. The State Department has sole authority to issue, limit, deny or revoke a passport.

Before contacting the State Department about revoking a taxpayer’s passport, the IRS will send Letter 6152, Notice of Intent to Request U.S. Department of State Revoke Your Passport, to the taxpayer to let them know what the IRS intends to do and give them another opportunity to resolve their debts . Clients must call the IRS within 30 days from the date of the letter. Generally, the IRS will not recommend revoking a taxpayer’s passport if the taxpayer is making a good faith attempt to resolve their tax debts.

Update: Control No.: TAS-13-0819-0014 Expiration Date: 08/13/2021 Impacted IRM(s): IRM 13.1.24

MEMORANDUM FOR TAXPAYER ADVOCATE SERVICE EMPLOYEES FROM: /s/ Bridget Roberts, Acting National Taxpayer Advocate

SUBJECT: Passport Advocacy Changes Caused by the IRS Commissioner’s Temporary Decision The purpose of this memorandum is to provide guidance to TAS advocates in response to a temporary change in how the IRS handles taxpayers working with TAS and who are subject to the Passport Certification Program.

The National Taxpayer Advocate has long advocated to exclude certain taxpayers with TAS cases from passport certification. She proposed that taxpayers coming to TAS certified would remain certified until TAS helped them obtain a statutory or discretionary exclusion. However, taxpayers who took steps to resolve their debt by seeking TAS help before certification would be protected from certification while working with TAS.

The IRS Commissioner Charles Rettig has not made a final decision on this proposal. He has agreed to temporarily suspend TAS cases from the Passport Certification Program. Effective July 25, 2019, all open TAS cases with a certified taxpayer will be systemically decertified. New TAS taxpayers will also be systemically decertified.

This means that until the Commissioner makes a final determination, all TAS taxpayers with at least one TAS IDRS marker on a balance due module will be protected from certification. Once the TAS case is closed and the TAS IDRS marker reversed, the taxpayer will again be eligible for certification if no other exclusion applies.

TAS will not incorporate this guidance into the next revision of IRM 13.1.24, Advocating for Case Resolution, as IRS Commissioner Rettig’s decision is temporary. New guidance will be issued once IRS Commissioner Rettig makes a final decision on this issue.

If you have any questions, please contact Michael Kenyon, Deputy Executive Director of Case Advocacy, Technical Support, at (701) 237-8299

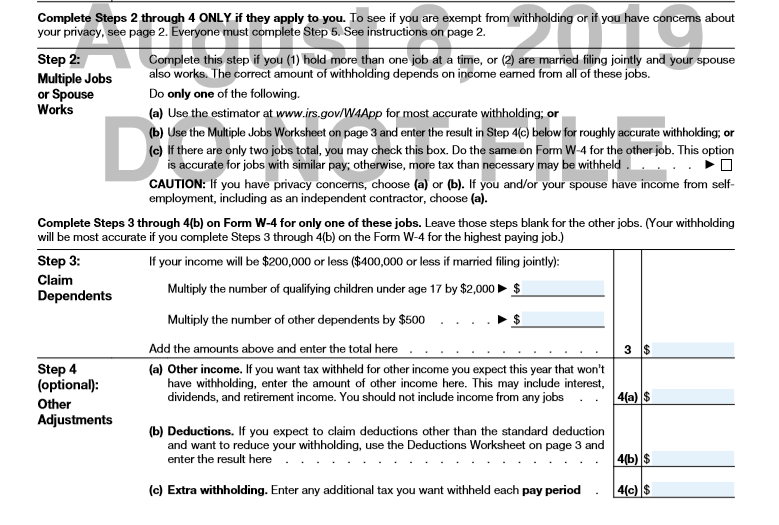

Issue 2: Issue 3: IRS, Treasury unveil proposed W-4 design for 2020 – Revised – Second Draft

The July newsletter unveiled the proposed New Form W-4 along with step-by-step instructions for completion.

According to the IRS, the new design reduces the form’s complexity and increases the transparency and accuracy of the withholding system. While it uses the same underlying information as the old design, it replaces complicated worksheets with more straightforward questions that make accurate withholding easier for employees.

This second version of the 2020 form has been released so that the programming of payroll systems can begin. The computation of withholding has not changed from the first draft 2020 Form W-4 and IRS expects the final version 2020 Form W-4 to be issued in the late-fall 2019. IRS adds that although the final version will not be issued for a few months, there will be no further substantive changes.

Changes contained in the second draft. The second draft changes the title of the form by removing the word “allowance.” The concept of withholding allowances, which was previously tied to the amount of the personal exemption, is no longer being used.

Some other small adjustments include changing the name of Step 2 from “Account for Multiple Jobs” to “Multiple Jobs or Spouse Works.” This step is for employees who hold multiple jobs at the same time or are married filing jointly and the employee and his/her spouse both work.

There is also a change for claiming exemption from federal income tax withholding for 2020. On the first draft, employees claiming such an exemption would write the word “Exempt” in box 4(d) of Step 4 “Other Adjustments (optional).” The second draft removes box 4(d) and instructs employees claiming exempt to write “Exempt” in box 4(c) of Step 4.

Step 2:

Step 2:

Introduces the new ESTIMATOR on IRS.gov and using the multiple jobs sheet.

The Internal Revenue Service launched the new Tax Withholding Estimator, an expanded, mobile-friendly online tool designed to make it easier for everyone to have the right amount of tax withheld during the year. The Tax Withholding Estimator replaces the Withholding Calculator. The new Tax Withholding Estimator offers workers, as well as retirees, self-employed individuals and other taxpayers, a more user-friendly step-by-step tool for effectively tailoring the amount of income tax they have withheld from wages and pension payments.

The IRS took the feedback and concerns of taxpayers and tax professionals to develop the Tax Withholding Estimator, which offers a variety of new user-friendly features including:

- Plain language throughout the tool to improve comprehension.

- The ability to more effectively target at the time of filing either a tax due amount close to zero or a refund amount.

- A new progress tracker to help users see how much more information they need to input.

- The ability to move back and forth through the steps, correct previous entries and skip questions that don’t apply.

- Enhanced tips and links to help the user quickly determine if they qualify for various tax credits and deductions.

- Self-employment tax for a user who has self-employment income in addition to wages or pensions.

- Automatic calculation of the taxable portion of any Social Security benefits.

- A mobile-friendly design.

In addition, the new Tax Withholding Estimator makes it easier to enter wages and withholding for each job held by the taxpayer and their spouse, as well as separately entering pensions and other sources of income. At the end of the process, the tool makes specific withholding recommendations for each job and each spouse and clearly explains what the taxpayer should do next.

The new Tax Withholding Estimator will help anyone doing tax planning for the last few months of 2019.

Client’s will need to gather the most recent pay stubs and their most recent tax return. The client will need to know their filing status and whether they are a dependent on another person’s return. In addition:

- Number of dependents claimed.

- How many jobs they had in 2019?

- Types of income, i.e. job, pensions, social security, interest/investment income etc.

- How often they are paid.

- The date of their most recent payroll.

- Amount of wages they expect to receive and any expected bonuses and overtime.

- Federal income taxes withheld from your last paycheck.

- Any deferred compensation, contributions to HAS or cafeteria plans.

- Any adjustments to income or tax credits.

Most of your clients will rely on you for these calculations. In short, your client may just continue with their current W-4 but when there is a change, they must use the new Form W-4. Expect a few calls to assist with the information needed.

Facts about the new Tax Withholding Estimator

Taxpayers can now use the new mobile-friendly Tax Withholding Estimator to make sure they’re paying the right amount of tax as they earn it throughout the year. It’s a user-friendly step-by-step tool to help taxpayers effectively estimate the amount of income tax they should have withheld from wages and pension payments.

Some facts about the new tool, it:

- Allows taxpayers to separately enter pensions and other sources of income.

- Makes doing a Paycheck Checkup easier for anyone who had an unexpected tax bill or a penalty when they filed this year.

- Allows taxpayers and their spouses to easily enter wages and withholding for each job they hold.

- Makes specific withholding recommendations for each job taxpayers and their spouses hold – clearly explains what they should do next

Also, those most likely to owe tax because they’ve had too little tax withheld include:

- Taxpayers who itemized in the past but now take the increased standard deduction.

- Two-wage-earner households.

- Employees with nonwage sources of income.

- Taxpayers with complex tax situations.

Issue 4: Enrolled Agent News

As this year’s enrolled agent renewal cycle has finished, the IRS is beginning its annual clean-up of enrolled agents who have social security numbers ending in 0, 1, 2, or 3 and did not renew. Enrolled agents who did not renew during the 2016 and 2019 cycles will be moved to terminated status. Those who did not renew during the 2019 cycle will be moved to inactive status. Beginning this week, the IRS will send letters to those affected advising them of this action.

An enrolled agent in inactive status can still submit a late renewal for approval with proof of continuing education credit. Any enrolled agent in terminated status must re-take the Special Enrollment Exam to apply for re-enrollment. If an enrolled agent disagrees and has a record of previously renewing, he or she should contact the number on the letter.

IRS announced on Aug. 2 that with the culmination of this year’s enrolled agency renewal cycle, it is beginning the annual clean-up of enrolled agents who have Social Security numbers ending in 0, 1, 2, or 3 and did not renew. Enrolled agents who did not renew during the 2016 and 2019 renewal cycles will be moved to terminated status, while those who did not renew only during the 2019 cycle will be moved to inactive status.

Issue 5: Automatic Estimated Tax Penalty Relief for 2018

The IRS is automatically waiving the estimated tax penalty for the more than 400,000 eligible taxpayers who already filed their 2018 federal income tax returns but did not claim the waiver.

The IRS will apply this waiver to tax accounts of all eligible taxpayers, so there is no need to contact the IRS to apply for or request the waiver. The automatic waiver applies to any individual taxpayer who paid at least 80% of their total tax liability through federal income tax withholding or quarterly estimated tax payments but did not claim the special waiver available to them when they filed their 2018 return earlier this year.

Refunds planned for eligible taxpayers who paid penalty

Over the next few months, the IRS will mail copies of notices CP 21 granting this relief to affected taxpayers. Any eligible taxpayer who already paid the penalty will also receive a refund check about three weeks after their CP21 notice regardless if they requested penalty relief. The agency emphasized that eligible taxpayers who have already filed a 2018 return do not need to request penalty relief, contact the IRS or take any other action to receive this relief.

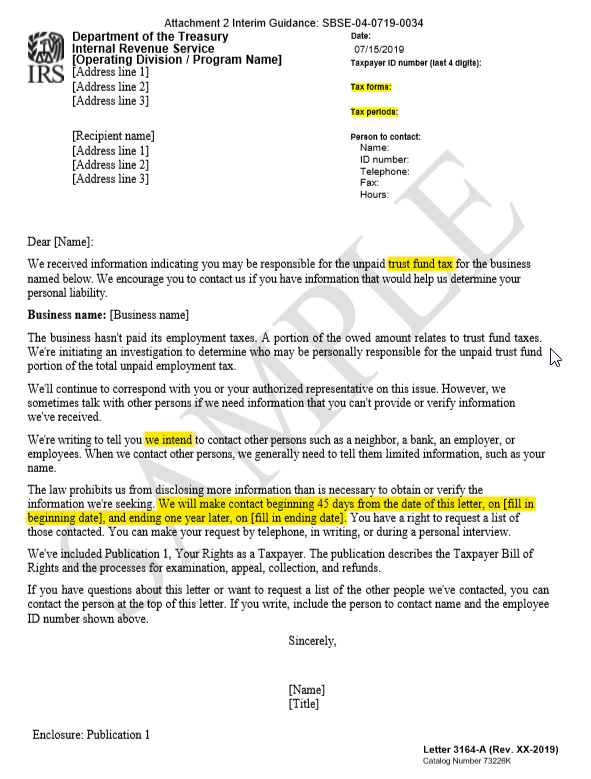

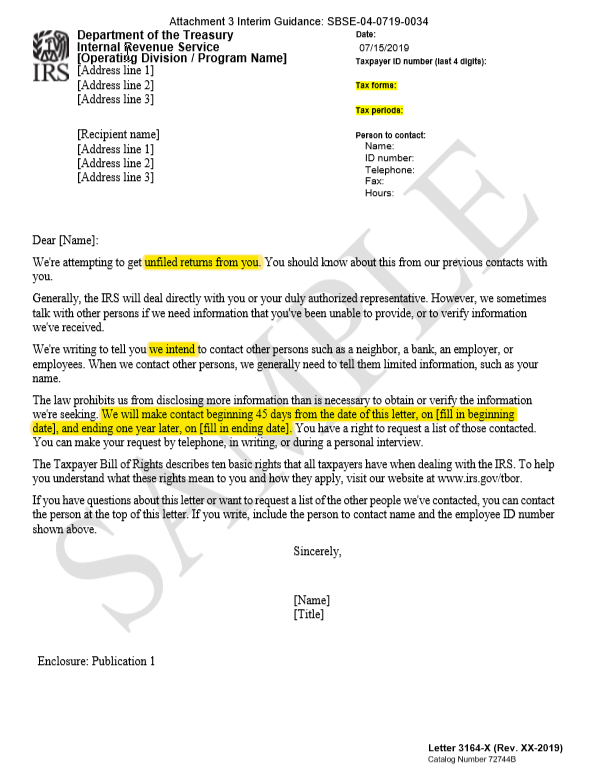

Issue 6: Taxpayer First Act of 2019 – SBSE 04-0719-0034

Three provisions of the Taxpayer First Act will go into effect in August 201 including:

- Additional limits on IRS summonses – the information sought must be narrowly tailored and pertains to the failure (or potential failure) of the person or group or class of persons referred to in the statute to comply with one or more provisions of the Code which have been identified.

- Designated summonses – before issuing a designated summons, the Commissioner of the relevant operating division of IRS and the Chief Counsel must review and provide written approval of the summons.

- Require earlier notice to a taxpayer when IRS contacts a third party – The Act provides that IRS may not contact any person other than the taxpayer with respect to the determination or collection of the tax liability of the taxpayer without providing the taxpayer with notice at least 45 days before the beginning of the period of the contact.

Two new letters have been created and are pending approval. Letter 3164-A (draft) and Letter 3164-X (draft). Both advise of possible contact with third party.

Effective August 15, 2019, Publication 1 will no longer satisfy the advance notice requirement of § 7602(c)(1).

The Code now requires that IRS:

- issue advance notice of third-party contacts,

- intend, at the time such notice is issued, to contact third parties (the notice must state this intent),

- specify in the notice the time period, not to exceed one year, within which IRS intends to make the third-party contact(s), and

- send the notice at least 45 days before contact with a third party.

In all cases involving third-party contact notices provided after August 15, 2019, or in which contacts with third parties will occur after August 15, 2019, a notice meeting the new requirements must be provided. Employees may not contact a third party until the 46th day following the date of the notice.

Issue 7: Draft 2019 Form 1041 available

The draft form contains a few changes:

- Includes references to new Form 1040-SR, U.S. Tax Return for Seniors;

- Adds a line item for the qualified business income deduction under Code Sec. 199A; and

- Adds a line on Schedule G to report the tax on electing small business trusts.

No instructions have not been released. Changes could still occur based on any comments or suggestions.

Issue 8: Draft 2019 Form 706, United States Estate (and Generation-Skipping Transfer) Tax Return – NEW ADDRESSES FOR MAILING

The new form is for decedents dying after December 31, 2018.

The only substantive change to the form is that Schedule R-1, has become a separate form, and has not yet been released.

The draft instructions also highlight new mailing addresses that became effective July 1, 2019.

- Forms 706 are mailed to Department of the Treasury, Internal Revenue Service, Kansas City, MO 64999.

- Amended Forms 706 are mailed to Internal Revenue Service Center, Attn: E&G, Stop 824G, 7940 Kentucky Drive, Florence, KY 41042-2915.

Issue 9: Ohio Enacts Tax Law Changes as Part of 2020-21 Budget

On July 18, 2019, Governor DeWine signed Amended Substitute HB 166, Ohio’s fiscal year 2020-21 budget legislation (HB 166). The new law contains significant tax law changes, including the following:

Individual Income Tax Reductions – Eliminates the bottom two individual income tax brackets and reduces tax rates for the remaining five individual income tax brackets by 4% for tax year 2019.

Changes to the Business Income Deduction (BID) – eliminated the BID for attorneys and lobbyists beginning in 2020.

Tax Credit Eligibility Changes – “Modified Adjusted Gross Income” is now defined as Ohio adjusted gross income plus any deduction for BID. Therefore, anyone using the following credits may be impacted.

- $20 personal exemption credit.

- Personal exemption deduction.

- Joint filing credit.

- Ohio dependent care credit.

- Retirement income credit.

- Credit for persons aged 65 years or older.

- Real property tax homestead exemption effective 2020 (2021 for manufactured homes).

In addition, Ohio Opportunity Zone Tax Credit has been changed. Ohio will only allow the credit once the investment is actually invested into the zone property, and Ohio increased the share of fund assets required to be invested from 90% (as with the federal credit) to 100%. Furthermore, Ohio will allow the credits to be transferred one time.

The Motion Picture Tax Credit was retained, but several changes were made around qualifying projects and companies.

Municipal Taxation of Supplemental Executive Retirement Plans (SERPs) – Beginning in 2020, Ohio has added definitions of pensions and retirement benefits plans for municipal taxation purposes.

School District Income Tax Base that employ “earned income” as their tax base, taxpayers must add back self-employment income and BID when computing taxable income.

Wayfair Sales Tax Updates – Ohio has updated their bright line nexus standards in light of the 2018 Wayfair decision. Taxpayers with greater than $100,000 of Ohio receipts or 200 separate transactions for the current or preceding calendar year must begin collecting Ohio sales tax effective August 1, 2019. In addition, Ohio enacted marketplace facilitator rules whereby the facilitator will be treated as the “seller.” As such, marketplace facilitators with Ohio nexus must begin collecting Ohio sales tax effective August 1, 2019.

Repeal of Sales and Use Tax Exemptions on the Following Transactions (Effective October 1, 2019):

Investment coins/metals and professional racing team purchases.

New Vapor Products Tax – Effective October 1, 2019, the new law enacted a tax on vapor products and implements the licensing of retail dealers of vapor products. The new tax is $0.10 per milliliter of vapor product. In addition, effective July 2020, manufacturers and importers of vapor products must also register and begin filing monthly reports with the state.

Issue 10: IRS Automatically Waives Estimated Tax Penalty for Eligible 2018 Tax Filers

The IRS is automatically waiving the estimated tax penalty for the more than 400,000 eligible taxpayers who already filed their 2018 federal income tax returns but did not claim the waiver.

The IRS will apply this waiver to tax accounts of all eligible taxpayers, so there is no need to contact the IRS to apply for or request the waiver.

Earlier this year, the IRS lowered the usual 90% penalty threshold to 80% to help taxpayers whose withholding and estimated tax payments fell short of their total 2018 tax liability. The agency also removed the requirement that estimated tax payments be made in four equal installments, as long as they were all made by January 15, 2019. The 90% threshold was initially lowered to 85% on January 16 and further lowered to 80% on March 22.

The automatic waiver applies to any individual taxpayer who paid at least 80% of their total tax liability through federal income tax withholding or quarterly estimated tax payments but did not claim the special waiver available to them when they filed their 2018 return earlier this year.

Refunds planned for eligible taxpayers who paid penalty

Over the next few months, the IRS will mail copies of notices CP 21 granting this relief to affected taxpayers. Any eligible taxpayer who already paid the penalty will also receive a refund check about three weeks after their CP21 notice regardless if they requested penalty relief.

Issue 11: Private Debt Collection Update

Before your client is contacted by one of the IRS approved private collection agency, they will receive two letters.

- The IRS will first send Notice CP40 and Publication 4518. These let the client know that their overdue tax account was assigned to a private collection agency.

- The private collection agency then sends their initial contact letter.

It has information on how to resolve the overdue taxes. Both letters contain a Taxpayer Authentication Number. It’s used to confirm the client’s identity. It’s also for the client to verify that the caller is legitimate. Client’s should keep this number in a safe place.

The four approved agenicies are as follows:

CBE P.O. Box 2217 Waterloo, IA 50704 800-910-5837

ConServe P.O. Box 307 Fairport, NY 14450 844-853-4875

Performant P.O. Box 9045 Pleasanton, CA 94566 844-807-9367

Pioneer PO Box 500 Horseheads, NY 14845 800-448-3531

When calling taxpayers, the PCAs will ask questions designed to make sure they are talking to the right person. The client should not provide any information to a caller before verifying that the caller has the correct Taxpayer Authorization Number (TAN) and using their IRS account transcript to verify that their account was sent to a PCA by the IRS.

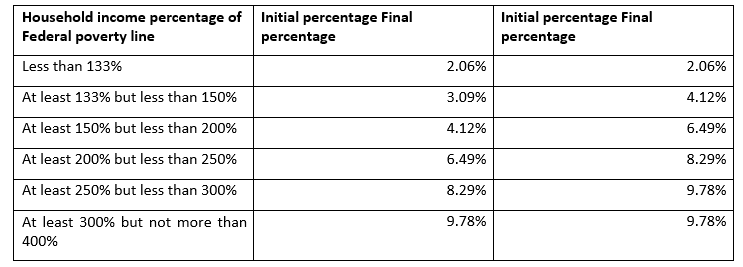

Issue 12: Applicable Percentage Table for 2020 Premium Tax Credit Calculation – Rev. Proc. 2019-29

For taxable years beginning in calendar year 2020, the Applicable Percentage Table for purposes of § 36B(b)(3)(A)(i) and § 1.36B-3(g) – Premium Tax Credit is:

Household income percentage of Federal poverty line:

Issue 13: REG-101378-19. Determination of the Maximum Value of a Vehicle for Use with the Fleet-average and Vehicle Cents-per-mile Valuation Rules

This document sets forth proposed regulations regarding special valuation rules for employers and employees to use in determining the amount to include in an employee’s gross income for personal use of an employer-provided vehicle. The proposed regulations reflect changes made by the Tax Cuts and Jobs Act, Public Law 115-97 (the Act).

If an employer provides an employee with a vehicle that is available to the employee for personal use, the value of the personal use must generally be included in the employee’s income under § 61 of the Internal Revenue Code. In addition, benefits paid as remuneration for employment, including the personal use of employer-provided vehicles, generally are also wages for purposes of the Federal Insurance Contributions Act (FICA), the Federal Unemployment Tax Act (FUTA) and the Collection of Income Tax at Source on Wages (federal income tax withholding).

- § 3121(a), 3306(b), and 3401(a).

The amount that must be included in the employee’s income and wages for the personal use of an employer-provided vehicle generally is determined by reference to the vehicle’s fair market value (FMV). However, the regulations under § 61 provide special valuation rules for employer-provided vehicles. If an employer chooses to use a special valuation rule, the special value is treated as the FMV of the benefit for income tax and employment tax purposes. §1.61-21(b)(4).

Two such special valuation rules, the fleet-average valuation rule and the vehicle cents-per-mile valuation rule, are set forth in §1.61-21(d)(5)(v) and §1.61-21(e), respectively. These two special valuation rules are subject to limitations, including that they may be used only in connection with vehicles having values that do not exceed a maximum amount set forth in the regulations.

Under the current §1.61-21 regulations (the final regulations), the vehicle cents- per-mile valuation rule may be used only to value the personal use of a vehicle having a value no greater than $50,400 (2019) (the sum of the maximum recovery deductions allowable under § 280F(a)(2) for the recovery period of the vehicle). §1.61 -21(e)(1)(iii).

The fleet-average valuation rule may be used only to value the personal use of vehicles having values no greater than $50,400 (2019). §1.61-21(d)(5)(v)(D). (The fleet-average valuation rule uses the term “automobile” rather than “vehicle.” Under the final regulations, each of these maximum values is adjusted annually pursuant to § 280F(d)(7).

Issue: 14 Domestic Partnerships and S Corporations Filing Under Proposed GILTI Regulations

Notice 2019-46, announced that the Department of the Treasury and the Internal Revenue Service intend to issue regulations that will permit a domestic partnership or S corporation that is a U.S. shareholder of a controlled foreign corporation to apply proposed §1.951A-5, related to the treatment of domestic partnerships and S corporations for determining the amount of the global intangible low-taxed income inclusion, for taxable years ending before June 22, 2019.

The notice also addresses the applicability of penalties for a domestic partnership or S corporation that acted consistently with proposed §1.951A-5 on or before June 21, 2019, but files a tax return consistent with the final regulations under §1.951A-1(e).

In order to apply the rules in proposed §1.951A-5 or for penalties not to apply under the notice, a domestic partnership or S corporation must satisfy certain notification and reporting requirements described in the notice. Prior to the issuance of the regulations described in the notice, domestic partnerships and S corporations may rely on the notice, provided they satisfy the requirements stated.

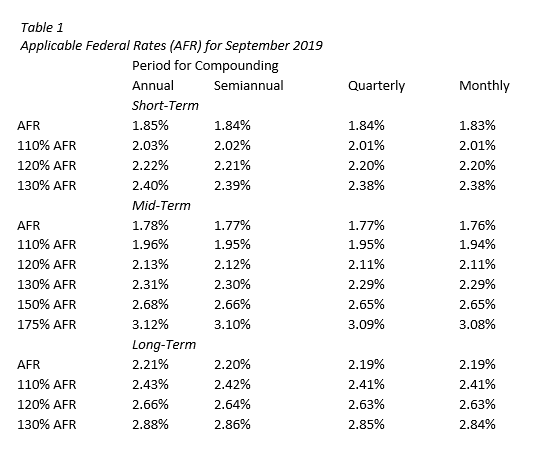

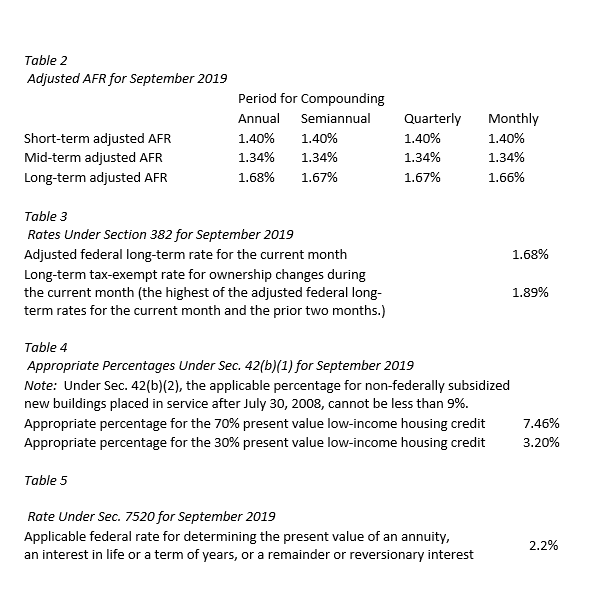

Issue: 15 Rev. Rul. 2019-20, 2019-36 IRB – Applicable Federal Rates for September 2019